In todays New York Times column about oil I criticized the economics professions remarkable lack of interest in trying to understand the energy crisis an event long past, to be sure, but a terrifically important event at the time, and possibly a model for crises future. In this note I want to enlarge briefly on some of the points I raised.

The mystery of the crisis

My guess is that if you asked a random economist about what happened in the 70s, he would answer that it is a story about the rise and fall of a cartel. But even at the time the alleged centrality of OPEC was questioned, and those questions remain just as valid today.

The basic problem with the cartel story was pointed out by a number of people, but perhaps most forcefully by Cremer and Salehi-Isfahani, in a paper circulated in 1980 but not published until 1989. Basically, OPEC did not, on the face of it, have the elements of a successful cartel. It was too fragmented culturally and politically how can you expect people to avoid price wars when, as history would soon show, they are quite prepared to engage in real shooting wars with each other? And the cartel didnt even engage in the most basic cartel behavior setting output quotas until 1982, that is, when oil prices were already under pressure.

The conventional answer to these criticisms is that there was a cartel within the cartel: Saudi Arabia and some of its neighbors engaged in output restriction, allowing OPEC to work. And there is something to that. But when you look at the Saudi-plus share of world output, it still looks suspiciously small. The Saudi output restrictions wouldnt have worked if other oil producers hadnt been very restrained in their own output, in some cases cutting it even before the introduction of quotas in 1982.

So what can explain the 12-year success in raising oil prices?

Multiple equilibria

Apparently in the late 70s a number of people began talking about perverse supply responses as an important element in the crisis. Cremer and Salehi-Isfahani wrote up that idea in a paper that for some reason did not have a lot of influence; but let me come back to that shortly.

The basic idea was that oil differs from ordinary commodities not in the existence of a cartel, but in three other facts: it is an exhaustible resource, production is controlled by national governments, and for the major oil exporters oil is the overwhelmingly dominant source of national income.

The fact that oil is an exhaustible resource means that not extracting it is a form of investment. And it is an investment that might look attractive to a national government when oil prices are high. If a country does not want to spend all of the massive flow of cash generated by a sudden price increase on consumption, it must do one of three things: engage in real investment at home, which is subject to diminishing returns; invest abroad; or "invest" by cutting oil extraction, and hence reducing supply.

Why not invest entirely abroad? There are a number of reasons, but one is surely political: as Iran and Iraq have found, assets abroad are vulnerable to seizure by the Great Satan.

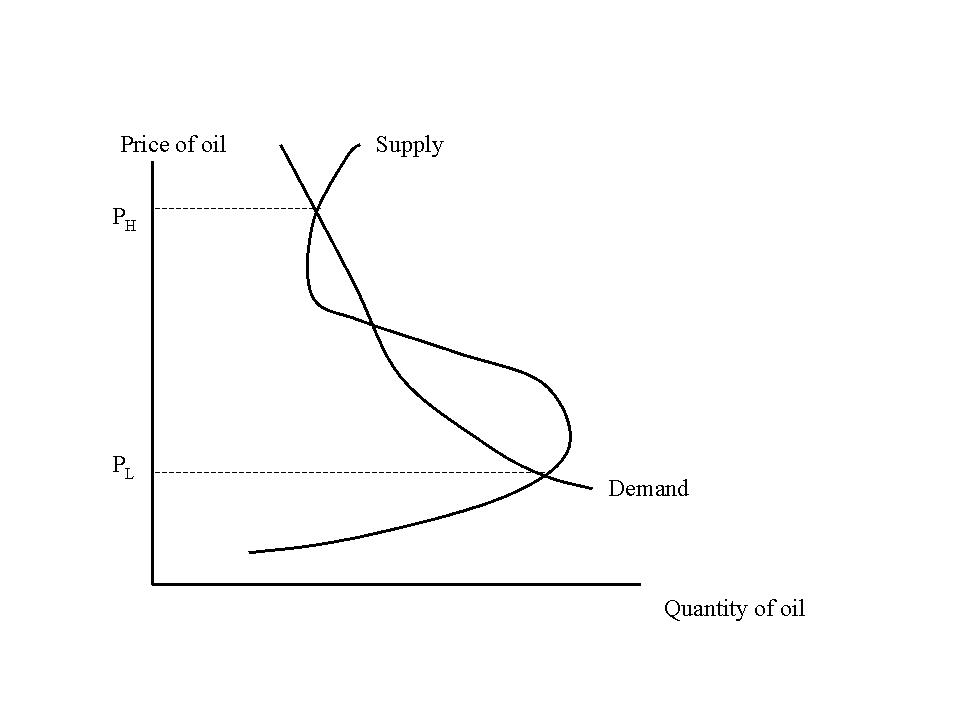

So there is a definite possibility that over some range higher oil prices will lead to lower output. And given highly inelastic demand, as Cremer et al showed, that means that you can have multiple equilibria. Figure 1 illustrates the point: given the backward-bending supply curve and a steep demand curve, there are stable equilibria at both the low price PL and the high price PH.

I might add that one need not believe in a perfectly competitive market. In fact, I suspect though I havent tried to do a formal model that a high price may make it easier for countries with some market power to sustain a quasi-cooperative equilibrium. For example, one might well believe that the discount rate is lower when countries are cash-abundant, and that this makes the future penalty for cheating that raises current income but risks the eventual collapse of the high-price regime loom larger.

Aside from the evident weakness of OPEC viewed as a cartel, the history of the rise and fall of oil prices is also it seems to me, as it also seemed to Cremer very suggestive of some sort of multiple equilibrium story. The original surge in oil prices came suddenly and unexpectedly, with a long-term effect from a short-term restriction of supply not what you would expect from a cartel gradually learning about its market power, but very much what you would expect if events "tipped" the market from one equilibrium into another. The collapse of oil prices in 1986 also came with dramatic suddenness, again suggestive of a collapse of one equilibrium and the establishment of another.

Why didnt the multiple-equilibrium view gain more acceptance? This is something of a puzzle. Perhaps it seemed too exotic at the time, especially applied in such a down-to-earth (below-the-earth?) industry as oil. Perhaps the elegance of Hotelling-type models was too seductive, even though they manifestly did not work very well. In Cremer and Salehi-Isfhanis 1989 and 1991 writings, there is a definite tone of puzzled exasperation with the lack of interest in their work.

What is particularly odd is that fancy, multiple-equilibrium stories are now very fashionable when applied to high-tech sectors. But everyone has lost interest in the old energy issue.

The energy crisis and other crises

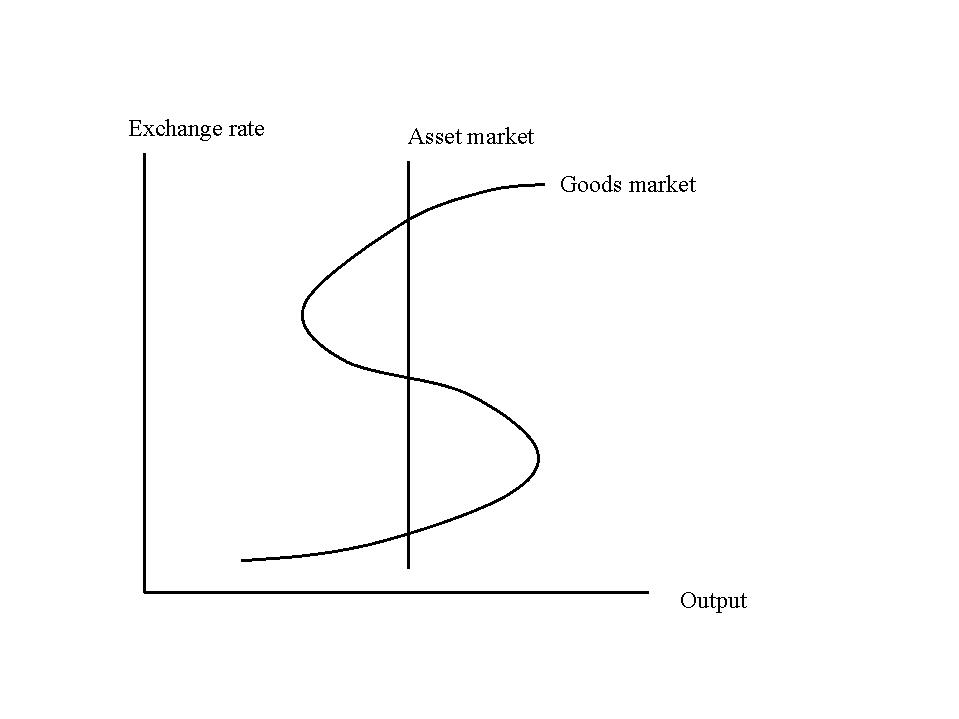

What struck me, on revisiting the modeling of the energy crisis, is its resemblance to the issues that arise in modeling the Asian financial crisis. There again the crisis appeared suddenly, surprising everyone; and there again the best stories involve some kind of multiple equilibria, perhaps arising from the balance-sheet effects of dollar-denominated debt. In my little summary paper Analytical afterthoughts on the Asian crisis , I showed how a stripped-down model along these lines could be represented with a diagram like Figure 2; the resemblance to Figure 1 is obvious.

There is another parallel with the energy crisis: now that the Asian crisis is past, people are quickly losing interest in it. It should, I believe, be viewed as an object lesson both in the importance of multiple-equilibrium stories in economics and in the potential instability of markets. But the profession is quickly turning aside to other questions, and reinterpreting the crisis if we think about it at all in more comfortable, less scary terms.

I guess crucial puzzles in economics never get resolved; they just fade away.