Electric Power Transmission: Rationing a Limited Resource

However, there is a catch. Under the new system, generators might not be located near their customers. As more electricity must be shipped longer distances, loads on the regional transmission systems are increasing, and sometimes those systems cannot cope. For example, some power lines may already be at capacity; lines may be unavailable due to maintenance activities; a storm or other natural event may bring a line or series of lines down; or proposed transfers of electricity may upset frequency or voltage. Despite such "constraints," the law says that all generators and customers must be given "equal access" to the regional transmission facilities needed to deliver electricity.

Dealing with this problem falls to the "central coordinator"--the entity that makes moment-to-moment adjustments to balance supply and demand, thereby ensuring the delivery of electricity at constant frequency and voltage. When the demand for transmission exceeds the capacity of the transmission system, the central coordinator must decide what action to take. Temporarily cutting off selected generators is one simple and obvious solution. But that approach does not provide equal access and is inherently unfair: any electricity entering the network merges with flows already on the network, so all participants contribute to any problem to some extent. An additional challenge for the coordinator is determining how much to charge for transmission services. A flat fee is inappropriate because the cost of transmitting a kilowatt is not always the same. For example, when flow on a line is high relative to its capacity, the line can heat up, pushing up maintenance costs and increasing the amount of electricity lost as it travels through the lines. Since some electricity is always lost in transit, sending a given amount of electricity to a distant customer is more expensive than sending it to a customer nearby.

Since the early 1990s, MIT researchers led by Dr. Marija Ilic have been studying problems and opportunities associated with the changing electric power industry. Building on decades of related research at MIT, Dr. Ilic's team has designed software and hardware for controlling operation of the network and has developed methods of establishing prices that would include not just generating costs but also the changing costs incurred in maintaining the network (see e-lab, October-December 1994).

Two years ago, Dr. Ilic teamed up with Francisco D. Galiana of McGill University to tackle competition-related transmission issues. To facilitate their research, Dr. Ilic, Professor Galiana, and their coworkers at MIT and McGill established an industrial consortium that not only provides financial support but also holds periodic workshops involving industrial and regulatory representatives. Interaction with those experts is critical: the concepts emerging from the MIT/McGill research differ so radically from other approaches to transmission provision and pricing that feedback from potential users and regulators is a must.

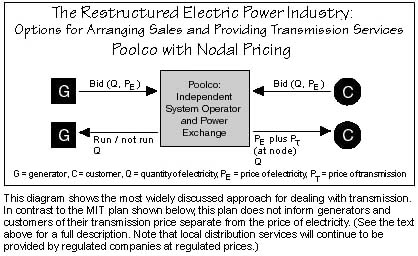

The most widely known approach now being proposed for dealing with transmission

is "nodal pricing." This method, based on work done in the 1980s by the

late Professor Fred C. Schweppe of MIT, assumes that the electric industry

operates as a "poolco"--a structure now emerging in New England and New

York, where multi-utility power pools have been strong. As shown in the

figure below, these poolcos act as the central coordinator, or "independent

system operator" (ISO), and also run the power exchange," a spot market

where day-ahead purchases of electricity from generators are arranged by

competitive bidding. Generators and customers submit bids to the ISO. The

ISO then informs generators whether they should run (the lowest-priced

generators are chosen first) and how much electricity they should produce,

and it tells customers how much electricity they will receive and the price

they must pay. The price for buying the electricity itself is bundled together

with a charge for transmission services and billed at the end of each day

or of each "transaction" between buyer and seller. The price for transmission

differs from one location, or "node," on the transmission system to another.

The difference in price reflects the distance of a node from generating

units, the capacity of the connecting wires, the level of demand, and other

factors that may limit transmission capacity and increase costs at that

node at a given time.

Reviewing the evolving state of the power industry nationwide, Dr. Ilic and her colleagues realized that assuming that the industry is structured as a poolco is too limiting. Indeed, other industrial structures are emerging in other parts of the country. For example, in California the ISO and the power exchange are not linked, as they are in a poolco. Instead, an independent entity runs the spot market and an ISO implements the completed deals with no knowledge of the electricity prices involved. And in the Midwest, the industrial structure is still up in the air. Some companies want to form a poolco, while others want to be free to make "bilateral" agreements--agreements made directly with their customers that would subsequently be implemented by an ISO.

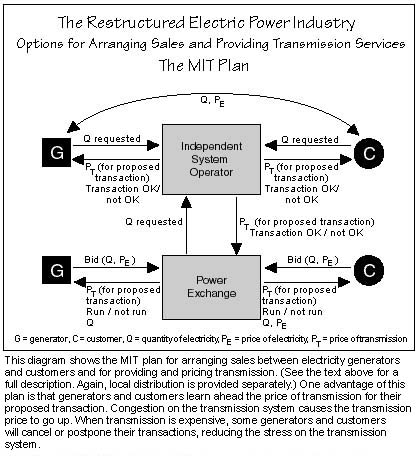

Dr. Ilic and her colleagues therefore reexamined the issues of transmission

pricing and provision without assuming a specific market structure.

As they developed their "MIT plan," one of their primary goals was to reduce

the control given to the ISO. Under nodal pricing, the ISO decides which

generating companies will provide the needed electricity--a decision that

directly affects the profits of market participants and limits the opportunity

for competition. Under the MIT plan, the ISO oversees the real-time operation

of the transmission system but not the dealings between the generators

and their customers. As the figure below shows, the ISO and the power exchange

are separate entities. Generators and customers can still submit their

bids to the power exchange (the bottom box), which runs the spot market.

Or they can deal directly with one another to make bilateral agreements

(shown at the top of the diagram). The power exchange and the bilateral

generators and customers then tell the ISO the amount of electricity (not

the prices) they would like to have transmitted.

The ISO must then deal with transmission and its pricing. If the transmission system cannot handle all the requested transfers of electricity, the ISO could accept some generators and reject others, informing those rejected of how to make other arrangements that will not threaten the health of the transmission system. But that setup would give the ISO too much power, so the MIT plan takes a different approach--an approach in which the ISO rejects or cuts off transactions only in emergencies.

On receiving the requests for transmission service, the ISO informs both the power exchange and the bilateral generators and customers of the transmission price associated with their proposed transaction. The quoted price reflects proposed rather than past activity. Thus, participants asking to get on the system--and those already on it--get signals indicating the transmission price they will have to pay. That price is based not on the node involved but rather on the specific transaction's contribution to any deterioration in overall system conditions. If, for example, a generator plans to feed a large amount of electricity into a line that is approaching its limit, the quoted transmission charge will be high. Knowing that charge, the seller and buyer can choose whether or not to implement the transaction--or they can go back later for a revised quote that will reflect the new conditions on the constantly changing transmission system. The closer the system is to becoming constrained and the more serious the impending problem, the higher the transmission charge.

This plan has many advantages over the poolco/nodal pricing approach. For one thing, it works in an industry that includes both spot market purchases and bilateral agreements. Supporting both types of deals is important: the spot market enables the ISO to make near-term adjustments in supply and demand, and bilateral agreements enable companies to hedge against swings in demand and price on the spot market. While nodal pricing bills customers for transmission after the fact, the MIT plan lets them know periodically what their transmission charges will be for the next increment of time (say, a day or a week ahead). And they have time to respond to the transmission price signals they receive. If demand gets dangerously high, the transmission price will be high and some users will choose to get off the system. As a result, the impending problem should be averted. The MIT plan thus creates a market that self-adjusts, decreasing the likelihood that constraints will occur on the transmission system. Moreover, simulations performed by the MIT team show that--assuming a competitive market--the prices and quantities in bilateral deals will gradually adjust so as to shift the transmission system toward more efficient operation. Thus, the ISO need not be responsible for efficiency. Market forces will do the job.

From a practical point of view, the MIT plan would be far easier to implement than nodal pricing would be. The price at a given node is supposed to reflect how much the activity at that node has moved the system away from its most efficient operation, that is, the scheduling of generators that would deliver the needed electricity at the lowest cost to the overall transmission system. Defining that "optimized" system is computationally extremely difficult--and for industrial structures other than poolco, conceptually hard. In contrast, the MIT plan calls for determining how close the transmission system is to a constraint and who is contributing how much to the potential problem. The MIT team has already developed software tools that can analyze current and projected flows on a transmission system and calculate appropriate price signals to deliver to potential generators and customers. To implement the software, the ISO can use real-time data from on-line information systems that are now required by the Federal Energy Regulatory Commission.

Finally, the MIT plan permits new ways of looking at the reliability of electricity supply. In the past, utilities tried to provide all customers with uninterrupted service--the highest level of reliability. To do so, they maintained excess capacity and costly backup systems that could be turned on quickly. All customers got high reliability--and paid a high price for it. Under the MIT plan, users are able to choose their level of reliability, cutting themselves off if prices become too high. Thus, the user that places a high value on reliability will pay a high price to get it, and the user that requires less-than-perfect reliability has a new opportunity to save money.

Another interesting question is what to do with the money that the ISO retains as a result of charging for transmission. Professor William Hogan and his colleagues at Harvard University suggest that the money--the "merchandise surplus"--be used to provide insurance policies for system users. Users would buy contracts guaranteeing their right to use the transmission system, regardless of its condition. If conditions on the system precluded a proposed transaction, the ISO would use the merchandise surplus to compensate the contract holder financially. In contrast, the MIT group believes that the merchandise surplus should be used to maintain and upgrade the transmission system. The transmission system now in place is barely larger than it was a decade ago, and much of it is old. Using the merchandise surplus to improve and expand it would mean that more transactions between generators and customers could be fulfilled without constraint.

The MIT and McGill researchers believe that power supply is not the

only task that could become competitive in the new electric power industry.

For example, utilities have traditionally maintained devices that operate

automatically to keep frequency and voltage on the transmission system

constant, despite the actions of generators and their customers. But they

received no specific compensation for buying or operating those devices.

In the restructured industry, other firms are beginning to offer those

"ancillary" services. The researchers are examining possible arrangements

whereby those emerging firms could also become players in the competitive

electricity market. And they are looking for the most efficient means of

compensating for transmission line losses. The ISOs could buy the extra

electricity needed to make up for those losses and pass their costs on

to customers. But more efficient approaches may be possible, perhaps involving

special generation-supply firms that act competitively--yet another

force to move the market toward lower costs and higher efficiency.