| Vol.

XVIII No.

3 January / February 2006 |

| contents |

| Printable Version |

MIT Retirement Plans: A Brief Summary

Click here for a quick overview of the new Pension Calculator.

Members of the faculty often acknowledge that they lack the time to monitor their progress towards retirement on an ongoing basis. The good news is information regarding MIT’s Retirement Benefits is becoming increasingly accessible and assistance is simply a phone call away. Whether you are just starting to save for retirement or retirement is imminent, MIT’s retirement counselors are available to provide you with information that will help you make informed decisions.

MIT’s retirement plans can help you build long-term savings and provide you with sources of income when you retire from the Institute. Both the MIT Basic Retirement Plan and the MIT Supplemental 401(k) Plan provide opportunities for you to plan for your future.

Basic Retirement Plan

The MIT Basic Retirement Plan is a defined benefit plan that provides you with monthly lifetime income at retirement. MIT pays the full cost for the plan and, if you are eligible, enrollment in the plan is automatic. You are vested in the Basic Retirement Plan after you are employed by MIT for five years. Your accrued benefit is determined in two ways and you receive whichever is greater:

1. Cash Balance Benefit (the 5% Account Method)

Under this method, a bookkeeping account in your name is credited with 5% of your pay each month. The account is also credited with interest. When you elect to receive your benefit, the balance in your bookkeeping account is converted to a monthly lifetime benefit (known as a single life annuity) which is based on certain assumptions about interest rates and life expectancy.

2. Career Average Benefit (the 1.65% of Pay Method)

Under this method, you earn an annual benefit equal to 1.65% of your pay received while participating in the Plan. This annual benefit assumes your benefit payments will start on your normal retirement date and will be paid to you for as long as you live, with no survivor benefits. Your normal retirement date from MIT is the first of the month following or coinciding with your 65th birthday.

If you have more than 10 years of service with MIT, you must take your benefit as monthly lifetime income (an annuity). There are many forms of annuities available to you when you retire, some of which allow you to have all or a portion of your benefit continue to another person (usually a spouse) after your death. The actual benefit payments you receive will depend on your age when benefits begin and the form of annuity you choose.

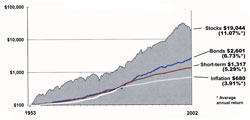

(click on image to enlarge)

Supplemental 401(k) Plan

The MIT Supplemental 401(k) Plan is a voluntary plan that allows you, if you are eligible, to contribute a percentage of your pay. MIT matches your contribution dollar-for-dollar up to 5% of your pay. You are always 100% vested in all 401(k) Plan contributions made by you and MIT. Federal law imposes annual dollar limits on your contributions: $15,000 for 2006 if you are below age 50 and $20,000 if on December 31st you are age 50 or older.

Similarly, it is important to note that federal law also limits the pay that can be considered for qualified retirement plans. In 2006, MIT only considers the first $220,000 of pay you receive.

| Back to top |

Prior Retirement Plan for Staff Members (RPSM)

If you are a faculty member who worked at MIT prior to July 1, 1989, you may have contributed to the Retirement Plan for Staff Members. In the RPSM Plan, you were required to contribute 5% of your pay while MIT contributed 10% of your pay. The balances that accumulated under this Plan transferred to the 401(k) Plan at Fidelity Investments. In fact, if you look at your most recent quarterly statement, you’ll see your RPSM balances are listed as separate sources.

There are two important provisions of the RPSM plan that exist today as part of the Basic Retirement Plan. If you are eligible, you are considered “grandfathered” for these benefits:

RPSM Early Retirement Supplement (ERS): An ERS, payable as a monthly lifetime annuity, is available to participants who earned benefits under the RPSM if they retire on or after age 60, but before age 65. You must have at least 20 years of MIT employment to be eligible for this benefit. The amount of the ERS will depend on your age when you terminate employment. The ERS benefit is $625 per month if you terminate employment anytime after attaining age 60 until the June 30th coinciding with or following your 60th birthday. Thereafter, the amount of the ERS decreases by $10.42 each month and is $0 after the June 1st following your 65th birthday. Although the amount of the ERS is determined by your termination date, the benefit is paid for the rest of your life, provided that you are not rehired at more than 50% effort.

RPSM Qualified Spousal Benefit (QSB): A QSB is paid as a monthly lifetime annuity to your “qualified” surviving spouse upon your death. The QSB is independent of the annuity option you elect for the MIT Basic Retirement Plan. Generally, your spouse is eligible to receive a QSB upon your death if you participated in the RPSM, and are at least age 55 with 10 years of retirement plan eligible service on the earliest of (1) your termination date, (2) your date of death or (3) the July 1st following your 65th birthday. Your spouse is considered “qualified” if you were married at least three years prior to the earliest of (1) your termination date, (2) your date of death, or (3) the July 1st coinciding with or following your 65th birthday. In addition, you must not be legally separated or divorced at the time of your death for your surviving spouse to receive this benefit. The amount of this benefit will depend on prior RPSM balances.

A reminder on Minimum Required Distributions…

Federal law states that you must begin receiving benefits from the MIT Basic Retirement Plan and the MIT Supplemental 401(k) Plan by the later of the April 1st following the year you turn 70½ or the April 1st following the year in which you terminate employment from MIT.

MIT’s Retirement Counselors are available to meet with you individually to discuss your MIT benefits as they relate to your overall retirement planning. We are located at the Benefits Office in E19-215. Please call 617-253-4272 to schedule an appointment. Paul Gunning, a Fidelity Investments senior retirement counselor, is also available to discuss your MIT Supplemental 401(k) Plan. To meet with Paul, please call him directly at (617) 258-8872.

| Back to top | |

| Send your comments |

| home this issue archives editorial board contact us faculty website |