| Vol.

XXIX No.

5 May / June 2017 |

| contents |

| Printable Version |

A Primer on Indirect Costs

and Why

They Are Important to MIT

Did you know that MIT subsidizes every research grant that it receives, even when the grant includes full overhead costs? The reason isn’t because MIT has a bloated administrative bureaucracy – as I will explain we’re actually organizationally lean. It's because MIT is a research-intensive institution, and conducting research is expensive.

Recent discussions in Washington about cutting the federal science budget by reducing indirect cost recovery should be deeply worrisome to all of us. Given the seriousness of the threat, I thought it would be beneficial for me to explain not only why these costs are important to MIT, but more importantly, how they benefit every research program at the Institute, including yours.

What are direct and indirect costs?

Research proposal budgets include direct and indirect costs. Direct costs are easily attributable to individual grants and include salary support for faculty, research staff, and postdocs working on the project, stipends for graduate students assigned to the grant, laboratory supplies, certain research equipment including computers, and travel and publication costs.

Indirect costs (IDC), aka the F&A (facilities and administrative) rate or overhead, represent genuine costs of performing research that are not easily attributable to individual grants. Think of these charges as applying to things that wouldn’t need to exist or be used as extensively if MIT didn’t conduct research. Examples include depreciation of research equipment and buildings, laboratory utilities (light, heat/cooling, power), hazardous chemical and biological agent management, libraries, internet, data transmission & storage, radiation safety, insurance, administrative services, and compliance with federal, state, and local regulations, e.g., Institutional Review Boards (RBs) for human subject or animal research. Note that only resources utilized for research are counted. The federal government partially reimbursesuniversities for these expenses.

Faculty salary support

In addition, since most faculty are paid in full by the Institute during the academic year, their participation in research during this time is supported by MIT.

How is MIT’s indirect cost rate calculated?

MIT's current indirect cost rate is 54.7%. This rate is set through Uniform Guidance 2 CFR 200, whereby universities calculate their actual overhead expenditures based on previous years and apportion them to various activities – research, instruction, or other. MIT’s rates are negotiated and audited each year and rates are applied only to those direct costs that are subject to overhead, which excludes tuition, equipment, major renovation, and repair and subcontract awards over $25K.

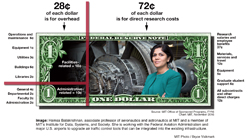

The easiest way to think about indirect costs, illustrated in Figure 1, is to understand how the average federal research dollar is spent at MIT. For a 54.7% overhead rate, 72 cents of every MIT research dollar goes to direct costs and 28 cents goes to indirect, or F&A costs. Figure 1 shows breakdowns within these categories and illustrates that a 54.7% indirect cost rate does not mean that 54.7 cents of every research dollar goes to overhead. It is 28 cents, because the rate is a fraction applied to the allowable direct costs added to the total direct costs.

(click on image to enlarge)

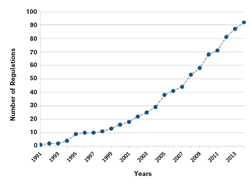

Dating back to 1991, the government implemented a cap of 26% of the total negotiated F&A rate for administrative costs. MIT has historically been under this cap (currently 19%, justifying my opening statement that MIT is administratively lean). Figure 2 shows that since that time, federal regulations and agency-specific requirements have skyrocketed, including dozens of new regulations and expansion of others (www.cogr.edu/sites/default/files/RegChangesSince1991_012417.pdf).

In principle, it would be possible to calculate the exact share of F&A costs required for each individual research grant, but it would be a logistical nightmare. Imagine tracking how much electricity was used for light, heat, and instrument operation on a project by project basis! UG 2 CFR 200 was designed to estimate these costs for all research projects over a year, limiting the need for complicated accounting.

What is under-recovery?

Many foundations either decline to pay indirect costs or reimburse them at much lower (typically 10%-20%) than the negotiated federal rate. Whenever a sponsor pays less than full F&A, it generates under-recovery (UR). Some institutions do not accept grants unless they carry full overhead, some write off the differential, and MIT, almost uniquely, identifies internal funds to cover the difference.

How has increasing investment in under-recovery helped our researchers?

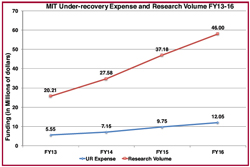

With federal support declining for over a decade, it was apparent that increasing foundation support that incurred UR would help sustain some areas of MIT’s research. Figure 3 summarizes how MIT has increased UR support. This investment includes contributions from my office, the Deans and DLCs. Figure 3 also shows the associated increase in research volume; clearly the increased investment has generated substantial funding. The slope of the funding curve is steeper than the investment because we have successfully negotiated higher rates from foundations in some instances, and in others we have been able to convert some costs usually classified as indirect to direct (e.g., facility costs).

While increased UR investment has helped, the desire to obtain such grants is growing at a faster rate than our ability to provide support.

(click on image to enlarge)

Why don’t we just forget about UR?

Some faculty have asked me – why doesn’t MIT just write UR off like some other organizations do? The reason is that UR is a real cost representing an investment that MIT makes in research. If we simply wrote it off, the benefit would fall to a limited cross-section of MIT researchers. Approximately 70% of foundation funding supports health-related research and the overwhelming majority is disease specific. By writing off these costs we would be helping researchers in those fields in an unbounded way, to the possible detriment of other areas in which research can’t be supported by UR. It is my goal to understand all of the ways that MIT could invest in research to enable informed, strategic decisions about how to best drive discovery.

What would happen if the government reduced indirect cost recovery?

MIT supports the need to assure that taxpayer dollars are invested responsibly. Federal agencies have different regulations, and while Uniform Guidance has provided some regularization, the burdens on grantees continue to grow (cf. Figure 2). If the government made an accelerated effort to reduce burdens leading to a decrease in administrative compliance cost (the “A” part of F&A in Figure 1), this would be a welcome development.

But if the federal government cuts indirect cost recovery without reducing administrative burdens, then, friends, we’ve got a problem. All of the facilities and services that are needed to carry out research will still be with us, and MIT will have to find other ways to cover the costs. Research support in the form of UR, cost sharing, graduate tuition subsidies, lab renovations, etc. comes from internal funds. These funds also provide support for most other things that MIT does, from salaries, to benefits, to start up and retention packages, to student support and beyond. So, it should be apparent why IDC recovery is important to MIT and to you personally.

If IDC are cut, wouldn’t all research universities be affected?

Yes, as would hospitals, laboratories, and research institutes. Those without sizable endowments would have a very limited capacity to make up the difference, but even institutions with larger endowments would have difficult choices to make.

What can we do to help?

MIT has been proactive in educating sectors, from government to industry to foundations to the public, on the importance of research and the role that indirect costs play. If you have contacts in states that don’t have major research universities, outreach in those regions would be particularly helpful. Voices of support from outside universities, particularly industry, are especially effective.

| Back to top | |

| Send your comments |

| home this issue archives editorial board contact us faculty website |