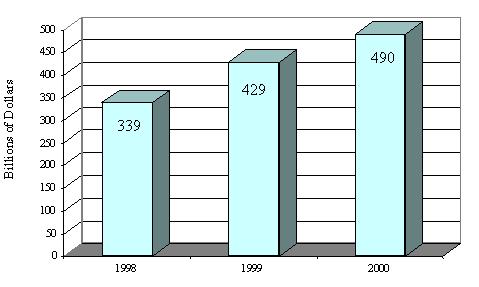

Now, the electronic payment is one of the "hottest" businesses because of the rapid market growth of electronic commerce and development of Internet technologies. Especially the business-to-business electronic payment can be one of the largest driving factors for the electronic commerce market growth as well as consumer electronic payment system such as e-cash, smart card and so forth. For example, the volume of transactions and the amount of payment per transaction are larger than those of consumer electronic payment systems are. This means if large enough number of companies participate in the business-to-business electronic payment, the providers of business-to business electronic payment scheme can have more business opportunities than those of other schemes (Figure 1-1).

Figure 1-1: Projection of Global Inter-business Electronic Commerce

.Source: Volpe, Welty &Co.

But at the same time, there are some concerns about the business-to-business electronic payment scheme. For example, now a lot of companies are using F-EDI (Financial Electronic Data Interchange) for business-to business payment, but the implementation cost of F-EDI is very high, and therefore, users are limited to large companies. Internet is expected to replace the F-EDI, but it has still some concerns about security and reliability.

This project will examine issues such as costs, security, reliability and so forth in business-to business payment schemes, and analyze how each scheme in the business-to business payment business will develop in the future, analyzing major players such as government, banks (Mellon Bank) and companies (ANX).