As it was mentioned in the prior section, only around 135.000 out of total of 6 million companies in the US are using electronic payments. The increase in the participation of America's corporations in electronic commerce activities is linked to their ability to perform electronic payments. Cost reduction and incentives are needed in order that F-EDI systems can become ubiquitous in the corporate world.

During this research project, two major processes have been identified as the major drivers to overcome the obstacles for F-EDI: 1) The regulations regarding payments exchanged between the Federal Government and Corporations and 2) The use of F-EDI on the Internet. Government along with banks and big corporations are the major players behind this initiative. In this section, some cases from the US. Treasury Department, The Mellon Bank and the Automotive Companies serve as examples of how the forthcoming future of business-to-business electronic payments is being articulated.

4.1 The US. Department of the Treasury (USDT's) and the Federal Procurement System

Currently, only half of all Federal payments are made electronically. The Government pays 6 cents to make an electronic payment compared with nearly 50 cents to make a single check payment. To reduce cost and as part of the President's initiative to promote electronic commerce, the 1996 Debt Collection Act was enacted by Congress. The act, mandates that all Federal payments be made electronically beginning in January 1999. This mandate is expected to save the Government as much as $ 500 million over five years.

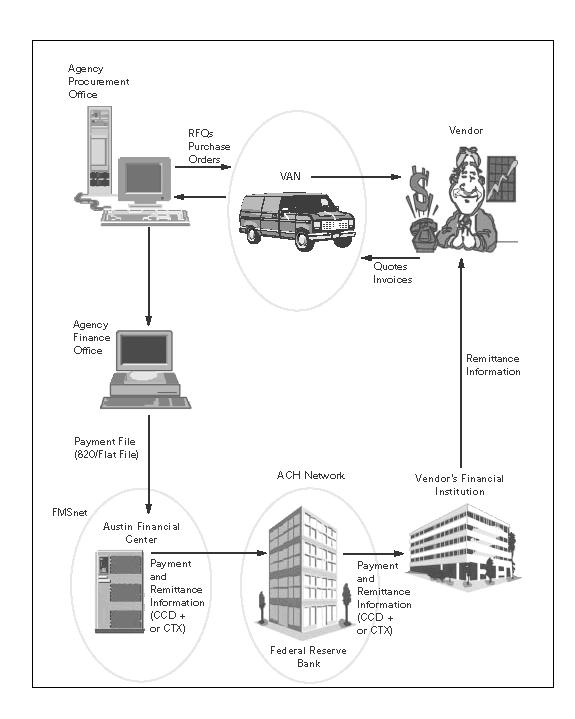

The Financial Management Service (FMS) is the organization within USDT's in charge of handling the Federal Government' payments. The majority of these payments are issued from the FMS Regional Financial Centers (RFC's). Although, non-treasury disbursed agencies issue their payments from Non-Treasury Disbursing Offices (NTDOs). The process that is now in place in the Government to handle its payments works in the following way (Figure 4-1):

a) The Federal agency procures goods or services from a vendor.

b) The Vendor provides goods or services to a Federal agency and submits an invoice requesting payment.

c) The Federal agency certifies payment to the vendor by submitting a payment request file with payment information to the agency's servicing RFC or, if a non-Treasury-disbursed agency, to the appropriate NTDO.

d) RFC or NTDO processes the Federal agency payment request file and transmits the payment to the Federal Reserve Bank.

e) The Federal Reserve Bank passes the payment file through the interbank network to the vendor's financial institution.

f) Vendor posts its accounts receivable from the payment and other information received from the financial institution.

Although the regulations deadline will act as a forcing incentive to increase the number of companies doing electronic payments it still resembles closely the advantages and disadvantages of the VAN F-EDI scheme. To improve the flexibility of the system and reduce the costs to the users, the Government is also working on initiatives to promote the use of more open arquitectures.

That is the case of a market trial of electronic checks being conducted by the USDT's Financial Management Service (FMS) since late 1997. The 12-month market trial is expected to demonstrate that using electronic checks over the internet is a secure and acceptable bank solution to electronic payments.

For the trial's duration, the electronic check is the payment method for 50 small to medium Department of Defense (DOD) contractors that previously received paper checks from the DOD. The pilot system involves the following steps:

a) The DOD receives invoices from participating vendors with Government contracts.

b) DOD instructs Treasury to write electronic checks to make payments, to digitally sign them and send them to the appropriate vendors via secure electronic mail, attaching as remittance information the DOD Advice of Payment.

c) The vendors use the remittance information to update their accounts receivable records. The vendors digitally endorse the checks and e-mail them, along with an electronic deposit slip, to a participating commercial bank. To endorse the check, a reader is used. The reader is a small, flat device not much bigger than a computer mouse that attaches to a PC serial port and enables users to digitally endorse and deposit electronic checks.

d) Once received by the bank, check and endorsement signatures are automatically verified. The deposit is credited to the customer's account and the electronic checks clear through an electronic cash letter presented to the Federal Reserve Bank, which handles account processing for the Treasury Department.

It can be seen that the implementation of this system requires minimal effort or investment. Users simply need the capability to send and receive e-mail and have an account at a bank that offers electronic check services.

BankBoston and NationsBank are commercial banks participating in the trial, along with the Federal Reserve Bank of Boston. Several technology companies developed underlying components. These include IBM and Sun Microsystems who developed the software to enable banks to process electronic checks using their existing paper check systems. IntraNet, Inc. was responsible among other things for the establishment of interbank clearing methods for the electronic payment mechanism. Research, Development & Manufacturing Corporation (RDM) developed the software that contractors are using to process their electronic check deposits. Readers have been provided by Information Resource Engineering (IRE), Inc. Finally, GTE Internetworking, RDM and Sun devised a program that was integrated with the government's legacy accounts payable system.

4.2 THE MELLON BANK AND THE INTERNET F-EDI

Other of the major obstacles that must be overcome in order to ramp-up the growth of electronic payments applications and hence electronic commerce is in the banking industry. Although some banks have offered for a long time F-EDI services, they usually rely on costly software and even more expensive VAN fees.

Mellon Bank Corporation, is a leader in the banking industry with around $1.6 trillion in assets. Its Cash Management Division, designs complete solutions of cash management services to meet the specialized treasury needs of middle market to large multinational corporations, government agencies, nonprofit organizations and financial institutions.

Mellon Bank has been an important player providing F-EDI under the traditional schemes. Mellon's strategy is to provide customers with comprehensive payable and receivable solutions. Recently, it has expanded its cash management services by replacing its mainframe-based F-EDI technology. Mellon's new F-EDI services are available under the name of Mellon RemEDI(R), and include a fully operational security solution for transmitting F-EDI documents over open networks, namely the Internet.

The new system is based on software provided by a company named Premenos, recently acquired by Harbinger (a VAN service provider). These software applications include Templar which was the industry's first deployable software to provide secure and reliable business-to-business EDI over the Internet.

Now, F-EDI provided by Mellon Bank includes a security service that gives customers confidentiality, integrity, authentication and nonrepudiation of both the origin and receipt of F-EDI messages. The use of this new technology allows Mellon to leverage the strengths of their traditional F-EDI systems, the use of TCP/IP networks, secure information and other Web technologies.

Major advantages of the new service offering include: 1) Faster turnaround on projects that require a company's data to be translated into national EDI standards, 2) Streamlined, easy-to-use setup procedures that reduce implementation time frames and 3) Being on the web, allows for faster implementation of new software releases that apply to F-EDI and EDI in general.

A concrete example of the gains was observed when Mellon Bank's performed a pilot project before adopting their Internet F-EDI. It took only 27 minutes for Bell Atlantic, a major customer, to send Mellon a 40MB file containing payment instructions via a T-1 line connected to the Internet. mainframe networks. This is a minimum cost if it is compared to using a VAN for transmission where the cost was estimated to be $20,000 and the transmission would have taken 43 hours for the same operation. Following Mellon are other major banks like Chase Manhattan who are going to the Web and creating real cost and convenience incentives for their trading partners to do the same.

4.3 Automobile Network eXchange, ANX

4.3.1 EDI in the automobile industry

EDI, Electric Data Interchange, was innovated in 1980s to facilitate data exchanging among companies. Like other industries, in automobile industry EDI connected manufactures and suppliers electrically and was very helpful for reducing errors by eliminating re-inputting order information or reducing inventory levels among all over supply chain by sharing production, inventory, or distribution schedule. EDI successfully re-organized the structure of supply chain.

But EDI was very expensive to install. EDI was a kind of closed network because the protocol for data exchange was not standardized and required costly investments in hardware, software, and private telecommunication links and data exchange. Thought this allowed suppliers which had installed EDI system and connected to the manufacture to enjoy the "entry barrier" for competitors, the barrier have been preventing small "second" or "third" tire suppliers from joining the supplier network.

This limitation of EDI has disabled automobile manufactures to expand its suppliers' computer network and utilize economies of scale.

4.3.2 Internet based-Ecommerce

On the other hand, current technologies such as TCP/IP(Transmission Control Protocol /Internet Protocol), Internet, or Web browser lowed the barrier for "second" or "third" tire suppliers or facilitated participating the suppliers' computer network because of its low cost and standardized technologies.

According to an exclusive purchasing survey, less than 46% of buyers currently use the Internet and the World Wide Web in the course of their jobs. Nearly 81% or buyers new have access to the Web. For them or even for others, the additional cost to utilize the Internet for Ecommerce is minimal.

4.3.3 Automotive Network eXchange, ANX

Among the first to adopt EDI, the auto industry has found that traditional EDI links, used for broadcasting order forecasts and manufacturing schedules, are technically limited and costly to operate, particularly for suppliers beyond the first tire. The industry, while not ready to give up on EDI, is hoping a new extranet, a private network that uses Internet technologies and functions much like the World Wide Web, will cut communication costs and speed the flow of information among supply chain partners around the world.

4.3.4 Automotive Industry Action Group, AIAG

Founded in 1982, AIAG is a not -for-profit trade association of more than 13,00 North American auto and truck manufactures and their suppliers. Originally recognized for its efforts to standardize electronic data interchange(EDI) and bar code standards to assist "first" tire suppliers, AIAG's mission has expanded to cover all levels of OEM supply chain.

4.3.5 Automotive Network eXchange, ANX

The Big Three US automobile manufactures (Chrysler, Ford and General Motors) and the Automotive Industry Action Group's (AIAG) recently began a pilot program for a Virtual Private Network (VPN) that will link the entire automobile production, sales and marketing process into one data communications network, ANX. Last year, the pilot program of ANX started and ANX services will be generally available in the third quarter of 1998.

ANX uses a common communication standard that will let authorized manufactures and suppliers share data through a single link. The network, which uses software "firewalls," user-specific passwords, and encryption technologies to keep data safe form hackers and nosy competitors, will allow auto makers and suppliers to securely transmit electrical data. The network covers the transmitting following information of doing business. - Electrical mail - Purchase orders - Shipping notice - Invoices - Computer-aided- design drawings - Performance rating updates by automakers ANX will consist of a number of certified service providers(CSPs), interconnected through a certified subset of the existing Internet exchange points. Each trading partner will connect to a CSP of its choice. Dealers, fleet buyers, and motor carriers could also be added to the ANX, further expanding communications among whole supply chain partners.

4.3.6 Effects of ANX

This network will be extremely variable for "second" or "third" tire suppliers which have not had an EDI connection to auto manufactures and have 100 or more different customers because EDI systems are scarcely implemented beyond the first tire suppliers. (If the supplier wants to connect to its customers with conventional EDI, it might require multiple connections to customers.) Because of the luck of key information such as production plan of manufactures or demand forecasts, "second" or "third" tire suppliers have had to hold safety inventory for fluctuating demand. By sharing the information, ANX is expected to solve the problem.

Actually, during the pilot program since last year, partners of ANX has cut leadtime by 58%, improve inventory turns more than 20% by sharing information, and reduced the order error rate by 72% by eliminating re-key data manually.

AIAG officials say the pilot demonstrated that North American automakers and their suppliers could cut their costs by $ 1 billion annually or an average of $71 per car in a 15 million vehicle year by simply improving communication through whole supply chain. This is realized by standardized technologies such as Internet or World Wide Web.

4.3.7 Payment system at ANX

As ANX just started last year, it does not cover the payment transactions among the network. At the pilot program of ANX, the customers receive invoices of the supplied goods from suppliers through the ANX and pay according to the invoices by conventional payment method like checks or new methods like Network F-EDI, VAN, or Internet. When a customer pays electrically, an actual transaction is done between banks representing the customer and the supplier through Inter Bank Network or ACH Network. Currently, the latter way of payment, electrical payment, is not very popular because ANX does not cover the option and only a few partners have F-EDI accesses.

But F-EDI is implemented on the ANX, huge impact on various aspects on each partner will be expected. Namely, immediate payments by F-EDI will reduce account payable and account receivable of each partner and improve cash flow. It will facilitate managing cash flow. Electric transactions by F-EDI will also eliminate paper work and reduce consequent cost. F-EDI is expected to be available on the ANX soon.

4.3.8 Future structure of automobile industry

This shift from EDI to Internet-based Ecommerce would change the structure of suppliers' network because any supplier may join the network, get the manufacture's information, and provide its own information with minimum cost and risk though the supplier needs to be authorized by the manufacture. Consequently, it would give the manufacture wider selection of suppliers and heighten the liquidity of suppliers' network. Current suppliers, which enjoy stable relationship with the manufacture, would be threatened by newly raising small suppliers. Competition among suppliers would be increase and prices of supplied goods would decrease.

Though manufactures have to pay attentions how to retain stable quality, quantity, price, and lead time of supplied goods among huge options, Ecommerce, especially Internet-based Ecommerce would change the structure of the industry. The movement of restructuring would be accelerate when electrical payment over Internet-based EDI, such as ANX, gets in use.

{kind=link}