| Vol.

XX No.

5 May / June 2008 |

| contents |

| Printable Version |

Endowment Spending Policy at MIT

The MIT Investment Management Company, or MITIMCo, coordinates the investment operations of the Institute. The department has the responsibility for the prudent stewardship of MIT’s long-term financial assets to ensure that they support the work of both current and future generations of scholars.

Principal among the investment assets supervised by MITIMCo are the endowed funds of the Institute. The many individual funds, whether for departmental support, scholarships, or otherwise, are collectively referred to as the Endowment, and are invested in a common investment pool referred to as Pool A, a shared investment vehicle similar to a mutual fund. Besides the endowed funds in Pool A, the staff at MITIMCo also manages the investment assets of MIT’s defined benefit pension fund, the Basic Retirement Plan, as well as a number of other significant pools of capital, including the Retiree Welfare Benefit Trust, the Life Income Fund gift program, endowed funds that invest separately from Pool A, and a number of operating funds of the Institute.

Management of MIT’s Endowment

In managing the Endowment, MIT keeps two primary goals in mind: providing a significant and stable flow of funds to the operating budget, and maintaining the long-term purchasing power of the principal. The first provides resources for today’s generation of scholars, while the second ensures that MIT will be able to deliver adequate resources to future generations of scholars.

To achieve its goals, MIT’s investments must generate high real rates of return. Unfortunately, high rates of return by their very nature often come with significant volatility. To reduce portfolio volatility without sacrificing return potential, MIT diversifies its portfolio by investing in high returning strategies and asset classes that are uncorrelated.

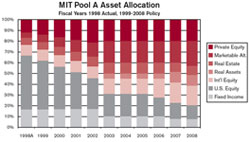

(click on image to enlarge)

Over the last decade, MIT has significantly improved the diversification characteristics of the portfolio. While in the late 1990s two-thirds of MIT’s investments were in U.S. stocks and bonds, today’s portfolio has only 20% in these asset classes, with the rest allocated to investments in alternative assets such as international equities, real assets, marketable alternatives (hedge funds), real estate, and private equity.

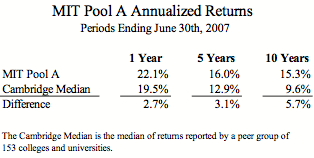

The combination of an increasingly well-diversified portfolio coupled with the strong performance of MIT’s investment managers has enabled Pool A to perform very well on both an absolute and relative basis.

Spending Policy

Endowment spending policy determines the annual flow of funds from the Endowment to the operating budget. A well designed spending policy takes for its conceptual framework the two principal goals of endowment management: providing a significant and stable flow of funds to the operating budget over the short-term to provide resources to this generation of scholars, while at the same time maintaining the purchasing power of the endowment over the long term, thus ensuring MIT will be able to provide adequate resources to future generations of scholars.

Unfortunately, achieving both these goals requires MIT to make trade-offs. Satisfying today’s scholars argues for consistent increases in spending unrelated to short-term Endowment performance to allow for steadfast programmatic support on an inflation adjusted basis. In severe bear markets, however, such a policy would result in disaster, as consistent spending increases would dramatically (and perhaps permanently) erode the purchasing power of the Endowment.

It is also true that excellent Endowment performance could cause problems if spending is not linked to changes in Endowment value. One can imagine the legitimate complaints from unhappy campus constituents who hear about great financial performance but are unable to enjoy its benefits.

Satisfying future generations of scholars, on the other hand, argues for spending that fluctuates directly with Endowment market value changes. Under a policy following this consideration exclusively, declines in Endowment value would be immediately followed by declines in spending, preventing erosion in long-term purchasing power and protecting resources for future generations. Unfortunately, this policy results in significant and disruptive volatility in the annual flow of funds to the operating budget and thus does not provide well for the current generation of scholars.

To balance the needs of all generations of scholars, MIT’s spending policy should both be responsive to changes in Endowment value and minimize year-over-year fluctuations in spending. The ideal spending policy acts as a shock absorber, keeping short-term spending relatively stable but gradually allowing changes in Endowment values to filter into changes in spending. A properly functioning shock absorber allows MIT to pursue investment strategies that generate high returns over the long term without unduly worrying about the short-term impact on the operating budget and allows the scholars of MIT to pursue educational and research work without unduly worrying about fluctuations in financial markets.

| Back to top |

Until recently, MIT employed a spending rule that buffered spending volatility by averaging changes in Endowment value over a three-year period and by targeting a distribution rate that varied between 4.75% and 5.5% of that average. While that rule served well for many years, its ability to buffer the operating budget from volatility in financial markets was overcome in the market decline of the early 2000s.

As a result, MIT has changed its spending policy to that of a Tobin spending rule. Named for James Tobin, recipient of the 1981 Nobel Prize in Economics, a Tobin spending rule sets the annual distribution in a particular year through a quantitative formula that has a “stability” term – the prior year’s spending adjusted for inflation – and a “market” term – the long-term sustainable rate of distribution times the market value of the Endowment. By selecting the weighting between these two terms, the Institute can determine the pace at which variations in market value are incorporated into spending. A heavier weighting towards the market value term provides greater responsiveness to rising – but also falling – markets. Conversely, weighting the stability term more heavily increases the buffering effect, sustaining the spending rate in the face of market declines, but slowing the response in market rallies. The new rule is shown below. Over time, MIT may adjust the inputs to best suit the Institute’s needs. We expect the adjustments to be infrequent to allow for thoughtful budgetary planning.

Distribution =

80% x (Distribution in Prior Year, Increased by Inflation)

+

20% x (5.1% x Market Value of Endowment)

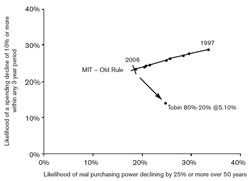

Evaluating the effectiveness of a spending policy requires that we measure the interaction of the chosen investment portfolio and spending rule over time. Monte Carlo simulation is well suited to providing these metrics. For the particular policy portfolio and spending rule under consideration, a Monte Carlo analysis projects the expected distribution of possible future Endowment return and spending outcomes, and measures the percentage that fail to meet our dual objectives. The short-term stability measure employed by the Institute is the likelihood that market declines would translate into a decrease in spending of 10% or more within any three-year period, termed a Short Term Spending Drop, or STSD.

Similarly, over the 50-year horizon of the analysis, we are concerned about the deterioration in the purchasing power of the Endowment by more than 25%, termed Long Term Spending Drop, or LTSD. These metrics give us some insight as to the likely performance of the portfolio-spending rule combination.

The chart shows how the spending rule employed by MIT over the last decade looked in LTSD-STSD terms. Notice that as portfolio diversification improved between 1997 and 2006 – providing greater return per unit of risk – the likelihood of both LTSD and STSD declined.

The chart further illustrates that the adoption of a Tobin spending rule can have a significant LTSD-STSD impact. We moved to the Tobin rule to reduce the historic volatility in the flow of funds to the operating budget. The analysis suggests that we have achieved this objective while "harvesting" the equivalent of only a few years of improved portfolio diversification.

| Back to top | |

| Send your comments |

| home this issue archives editorial board contact us faculty website |