| Vol.

XX No.

5 May / June 2008 |

| contents |

| Printable Version |

A Primer on Indirect Costs

Among university faculty, indirect costs or overhead has about the same appeal as taxation among political candidates. So it seemed appropriate, soon after April 15 in an election year, for me to offer some information about indirect costs, where they come from and how they are computed.

Indirect Costs

The rules under which the federal government reimburses universities like MIT for the costs of sponsored research are governed by Circular A21 from the Office of Management and Budget, “Cost Principles for Educational Institutions” [www.whitehouse.gov/omb/circulars/a021/a021.html]. The principles apply to “grants, contracts and other agreements” and “are designed to provide that the Federal Government bear its fair share of total costs.” A different set of rules applies to for-profit companies (a 2000 RAND study [Goldman, C. Williams, T., Paying for University Research Facilities, RAND, 2000] concluded that university overhead is lower than that of industry). The policy of A21 is to recognize and encourage the unique way each institution chooses to conduct research.

A21 distinguishes direct costs (faculty summer salaries, RA stipends, equipment, lab supplies, etc.) from costs associated with facilities and administration (F&A), also called indirect costs or overhead. F&A costs (operation and maintenance of buildings, capital depreciation, departmental and central administration, etc.) cannot be readily and specifically attributed to a given activity (e.g., instruction vs. research), nor to a specific sponsored project.

There are strict categories of allowed F&A costs and rules for allocating a fraction of these to organized research, in contrast, say, to instruction or other institutional activities.

Studies [Ibid; Report of Working Group on Cost of Doing Business, Council on Government Relations, 2003] have shown that the cost allocation rules generally favor the sponsors over the institutions, who end up absorbing a fraction of the expenses plausibly associated with organized research. One clear example, which affects many institutions, is an arbitrary cap set on the reimbursement of administration costs (the “A” of F&A; MIT’s A rate has historically fallen below the cap anyway). That cap has not prevented the government from imposing a continually increasing load of regulatory, compliance, and reporting requirements on the grantee institutions.

The organized research category includes all research activities, whatever the funding source, that “are separately budgeted and accounted for.” Any research effort with a budget, statement of work and/or deliverables, must be included in organized research. The fair share principle then F&A costs to each and every organized research activity, regardless of the source of funding. In other words, the federal government insists that each sponsor of organized research, including the university itself, pays its appropriate fraction of the F&A costs, or rather that the government pays no more than its appropriate fraction (this can result in the phenomenon of under-recovery described below).

The single metric for allocating “fair shares” to various award sponsors is money. More specifically, it is the direct expenditures covered by that award less a few specific items (RA tuition, larger subcontracts, and capital equipment), yielding modified total direct costs (MTDC). Because indirect costs are assessed on a transaction-by-transaction basis for every relevant MTDC expenditure, there is a misconception that overhead is meant to cover the "back office" costs associated with that transaction. Instead, it operates more like the Massachusetts sales tax.

The allocation of indirect costs requires a long process of detailed accounting following the rules of A21 (this process, indeed everything described in this article, is frequently audited within MIT and by federal and independent auditors). Every relevant expense is accounted for, put in the appropriate cost category, or cost pool, and then allocated (the result fills a fat notebook of spreadsheets every year). The allocation of a fraction of a given cost pool to the category of organized research vs. other activity categories is computed using a specific metric that can be readily determined for that category, such as square footage (for cost pools associated with space) or relative expenditures (say, for departmental administration).

The total MTDC and indirect cost expenditures are computed exactly after the close of each MIT fiscal year. Rates for current and future years are based on detailed estimates and projections. For MIT FY2007, which closed on June 30, 2007, the total direct costs of research (TDC) was $408M and, after appropriate deductions, MTDC was $253M. (These and all of the numbers in this article refer to on-campus research – the off-campus rate is calculated independently.)

(click on image to enlarge)

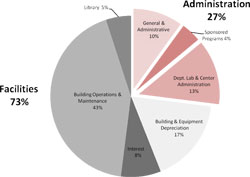

The total of all indirect expenditure cost pools for MIT FY2007 was $456M, of which $180M (40%) was attributed to organized research (the other 60% is paid with general Institute funds). Of the $180M, $131M (73%) are costs related to facilities, of which $73M is for operations and maintenance including utilities. The administrative indirect costs attributed to organized research are $49M (27%). This, in turn, is roughly equally divided between central administration, including administration of sponsored programs, and administration of departments, labs, and centers.

| Back to top |

The F&A Rate

The F&A rate for a given year is computed by dividing the amount of indirect costs attributable to organized research by the total MTDC, (e.g., for FY07, $180M/$253M). Fluctuations in MIT’s actual F&A rate can come from changes in both the numerator (costs) and denominator (MTDC). Over the past ten years facilities costs have doubled, primarily due to rising energy costs and the expenses associated with new buildings and major renovations. In contrast, administrative costs grew by 26% over 10 years, six points fewer than the growth in the Consumer Price Index for that period. MTDC also increased through the first part of this period, but then stagnated for the past five years, reflecting the stagnation in federal research funding. The combination reduced the actual F&A rate in the early years of this decade, but then drove a steady increase from FY2002 to FY2007.

Computed retroactively for MIT FY2007, the actual F&A rate was 71.1%. This exceeds the 65% rate that was billed to sponsors during FY2007, which had been negotiated early in 2006 with our cognizant federal oversight agency, the Office of Naval Research (ONR). Our billed rate for FY2008 is 67% and the provisional rate for FY2009 is 68%.

In total, indirect costs represent about 30 cents of every research dollar. Thanks in part to some changes in depreciation accounting and anticipated MTDC growth, the real F&A rate is expected to decrease and come more into line with the billed rate.

MIT is one of a small number of universities that can carry forward to future years the accumulated difference between the actual and billed recovery. This allows us to make moderate changes in the billed F&A rate that smoothes over the more rapid fluctuations in the actual rate. Over the years, the carry-forward has alternated between being positive and negative.

Under-recovery

Many foundations severely limit the amount of indirect costs they are willing to pay. Because the federal government understandably insists that it will not pay more than its “fair share,” MIT is required to supplement such foundation awards to cover full F&A costs at the billed rate. In other words, when MIT gets an award without full recovery, desirable as that may be for many other reasons, it causes us to “lose” F&A revenue whether or not the activity actually incurs extra indirect costs. As a simplified illustration, assume our MTDC and F&A costs were $200M and $100M, respectively, and all awards had full recovery at the computed rate of 100/200=50%. Now repeat the scenario but add one additional grant from Foundation X that pays $2.0M in MTDC, does not increase our actual indirect expenditures (this can only hold on the margins, of course), but pays zero F&A recovery. Because the total MTDC is now $202M the rate we can charge fully-paying sponsors falls to 100/202=49.5%, so we now recover only $99M from those sponsors. MIT must make up for the lost $1M from its own general funds. On average, of course, additional awards will increase indirect expenditures and will also affect the allocations of the cost pools, but the fact of under-recovery remains. In effect, MIT must provide $1M in cost-sharing to accept $2M from Foundation X.

Because under-recovery is a real cost, MIT policy requires that it be allocated to one or more faculty, department, School, or central budget. That means under-recovery support will inevitably compete with other priorities, including student financial aid, faculty start-up costs, renovations, and other educational or research initiatives. In recent years, the Provost has allocated more resources for under-recovery support, as have department heads and deans. In FY07, MIT spent over $5M to cost-share under-recovery.

Comparing to our peers

Although most universities are overseen by the Department of Health and Human Services rather than ONR, as we are, both agencies apply the exact same rules specified in A21. The one distinction is MIT’s ability to carry forward shortfalls or overpayments in F&A to future years (A21 allows this but most institutions have agreed instead to accept a single, predetermined rate with no carry-forward).

Institutions do differ on how they talk about F&A recovery and sometimes employ language that might cause confusion. For example, while A21 mandates that universities can only recover costs actually incurred by the institution, some universities talk of “returning” a fraction of their recovery revenue to a unit or even a PI. In some cases, the unit (e.g., a medical school) paid the F&A costs, so the allocation is still reimbursement. In other cases, this is really a strategy for allocating general funds to a unit in proportion to its research activity. Such strategies are easier to implement in some state institutions, for example, where a fraction of indirect expenditures might be covered by separate budgets that do not require reimbursement, making the recovery look like new revenue.

Regarding awards from foundations, every institution has to cost-share the F&A shortfall exactly as we do. Unlike MIT, however, most of our peers choose to absorb the additional costs either centrally, or at the School level without explicit budgeting.

Like MIT, most of our peers recognize under-recovery as an increasing drain on their general funds, and some are moving to set limits on how much they will accept. All of us are trying to educate foundation leaders about the reality of indirect costs, and some of us have policies for direct charging some F&A items, like the operation of facilities.

One thing to bear in mind is that, in comparison with peer institutions, MIT’s total revenues from research are a larger fraction of our on-campus annual operating budget, about 40% compared to ~30% for Stanford and UC Berkeley, and ~20% for Harvard (in 2006; excluding hospitals). The F&A recovery represents more than 10% of MIT’s campus operating budget and is nearly equal to the net revenue from undergraduate and graduate tuition combined. So MIT has somewhat less leverage for applying general funds to offset shortfalls in F&A than do some of our peers.

The F&A rates of all universities evolve over time, with the episodic building of new buildings and facilities and the ebb and flow of large and small research activities. The combination of circumstances noted above have currently placed MIT’s rate among the highest of our peers, something we are working hard to address. Luckily, other costs of research, like the employee benefits rate, are among the lowest, and we have just increased the RA tuition subsidy by five points.

Conclusion

As a long-standing PI supporting a research group in the face of declining NASA budgets, I well understand the pressure that our F&A rate places on faculty and research staff. The central administration has worked hard to control costs, make critical investments that will enhance research, and increase allocations for under-recovery. We welcome your comments and suggestions.

| Back to top | |

| Send your comments |

| home this issue archives editorial board contact us faculty website |