| Vol.

XIX No.

2 November / December 2006 |

| contents |

| Printable Version |

Financial Foundation for MIT's Future

MIT’s financial structure and recent history

MIT has seen significant increases in its overall financial resources over the last decade. As a result of growth in financial markets and extensive fund raising campaigns, the Institute’s net assets increased from $2.5B at the end of FY1996 to $10.1B in FY2006, representing a cumulative annual growth rate of 14.8%. At the same time, as a result of increases in instructional activity and sponsored research, MIT’s annual operations have almost doubled during the same period, increasing from $1.2B in FY1996 to $2.2B in FY2006.

(click on image to enlarge)

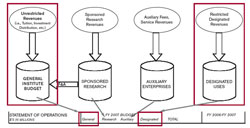

While net assets have grown roughly twice as much as operating expenses, the availability of financial resources has been asymmetrical across MIT ’s four operating categories: General Institute Budget (GIB), Sponsored Research, Auxiliary, and Designated (see Figure 1). The GIB funds the bulk of the academic MIT enterprise, and includes unrestricted funds that can be used for any Institute purpose. Its largest sources are tuition, unrestricted endowment income (e.g., payout to unrestricted accounts invested in Pool A), and facilities and administrative cost recovery. Sponsored Research represents the direct component of grants and contracts, typically controlled by individual principal investigators. Auxiliary includes proceeds and expenses from Housing, Dining, MIT Press, Endicott House, and Technology Review. Finally, Designated corresponds to restricted expendable gifts and endowment income paid to the holders of restricted Pool A accounts such as Professorships or Scholarships. Both the restricted and unrestricted endowment incomes come from annual distributions from restricted and unrestricted accounts, respectively, invested in Pool A. The Executive Committee of the Corporation votes these distributions annually, and they are typically referred to as “voted endowment distribution.”

MIT has generally viewed Sponsored Research and Auxiliary activities as self-funded. Since these budget categories do not fundamentally affect the Institute’s financial flexibility, the remainder of this article will focus on the GIB and the Designated funds.

Designated funds cover expenses that are within the scope of restrictions imposed by their donor or custodial academic unit.

As a result of the limitations on their use, as well as conservative spending and the desire to save for a rainy day, Designated resources available for spending are rarely exhausted and their aggregate balances have accumulated with time.

MIT’s continued need to maintain its competitiveness has put pressure on the GIB. As a result, the GIB expenses have been higher than the GIB revenues for the last several years, creating a structural budget gap within the GIB. In April 2000, the Executive Committee of the MIT Corporation authorized an “additional endowment distribution” of up to $500 million for the 2001-2010 period to finance strategic investments – that is, it authorized support from the endowment beyond that of the voted endowment distribution described above to close the budget gap resulting from these strategic investments and growing operating needs.

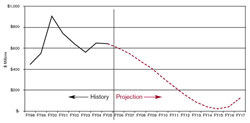

The additional endowment distribution has been provided by selling unrestricted endowment units in Pool A, normally referred to as the “quasi endowment” (see Figure 2). These financial plans formalized a longer-term trend that can be traced as far back as the early 1970s and well into the 1990s. Since then, MIT has closed annual budget gaps with unrestricted funds.

Protecting MIT’s Financial Flexibility

A significant fraction of the income from the voted endowment distribution is not available to help balance the GIB, as it is either held primarily by Departments, Labs, and Centers (DLCs), or is restricted by donors to specific uses. Moreover, in FY06, less than 10% of the endowment was sufficiently unrestricted to be considered quasi endowment and used to support the additional endowment distribution.

Figure 2. General Unrestricted Expendable Assets (Quasi Endowment)

(click on image to enlarge)

Given projected levels of fundraising and anticipated operating needs, our current financial practice is unsustainable in the long run. In fact, based on current projections, the Institute would have exhausted its unrestricted endowment funds by Fiscal Year 2015 (see Figure 2).

| Back to top |

FY08: Laying a New Financial Foundation for the Future

Strategy Description

Starting with Fiscal Year 2008, we plan to lay a new foundation for MIT’s financial future, increasing the Institute’s long-term financial flexibility by allocating funds more effectively between the GIB and the Designated operating categories.

The proposed strategy is essentially a “zero-sum game.” The plan will eliminate the additional endowment distribution by increasing the voted endowment distribution by an equivalent amount (see Figures 3 and 4). Whenever possible and allowable, the additional funds that academic units receive from the increased voted distribution payout (see Figure 4) will be exchanged with GIB funds. As a result, the aggregate GIB and endowment revenue to each DLC will be at least the same as before. In fact, as discussed below, the revenue to some DLCs will actually increase. Importantly, the proposed strategy does not increase MIT’s overall reliance on the endowment. It simply wraps the additional endowment need into the voted distribution, keeping the aggregate distribution from endowment funds at the same level as projected using the current model.

(click on image to enlarge)

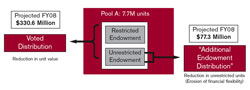

This new strategy will support the projected operating costs for FY2008 by first increasing the voted Pool A distribution, and then utilizing the lion’s share of the increased distribution to offset an equivalent reduction in support from the GIB. Let me contrast the new model with the current model: If we were to follow our current financial model of “voted” and “additional” endowment distributions, the voted distribution for FY08 would be ~$43 per unit, and a projected FY08 operating gap of about $77M would require an additional distribution derived from selling unrestricted Pool A shares (see Figure 3).

(click on image to enlarge)

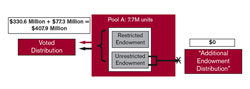

However, by increasing the voted distribution to $53 per unit, the operating gap is reduced to a nominal amount (see Figure 4). We plan to eliminate the use of the additional distribution entirely by FY09.

In sum, this strategy would eliminate MIT’s reliance on unrestricted endowment assets to balance the operating budget – a use that is unsustainable in the long term – while maintaining the same level of projected funding for academic units.

Of course, donor restrictions appropriately constrain the application of this rebalancing mechanism, and distributions from restricted funds can be exchanged for equivalent GIB funds only when such use lies within the restrictions of the funds.

While this and other limitations make a 100% exchange unattainable, discussions with the top 20 academic department holders of Pool A accounts indicated that a large portion of the increased voted distribution can substitute for today’s GIB funds.

The Strategy in Action

Endowment holdings are projected to include 7.7M Pool A shares in FY2008. Of these, 4.2M shares are in unrestricted and Scholarship & Fellowship accounts, which fund the GIB; 3.5M shares are in other restricted accounts that fund the DLCs. Increased voted distribution from the 4.2M shares will directly offset the need for additional distribution to the GIB. Increased voted distribution from the 3.5M of DLC-targeted funds will be used to offset a reduction in GIB allocation to the DLCs.

As an illustration, consider Undergraduate Scholarships. MIT accepts students on a “need-blind” basis and commits to meeting the full financial need of all students. In FY2006, total undergraduate financial aid expenditures amounted to $54M. Endowment income paid to Scholarship Funds covered only $36M, which left a gap of $18M that was covered by unrestricted GIB monies. Scholarship funds hold 1M Pool A shares, and implementing the new policy would have increased the endowed financial aid funding by $10M, therefore reducing the need for GIB subsidy from unrestricted funds to only $8M.

| Back to top |

The Strategy’s Impact

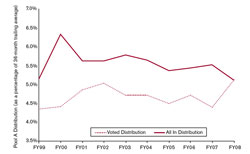

MIT’s Pool A Distribution Rate

The main purpose of MIT’s endowment is to provide a level of revenue stability for current and future generations of MIT faculty, staff, and students. To ensure that the purchasing power of the endowment is maintained for future generations, MIT has used as its target for the voted endowment distribution a spending range of 4.75-5.5% of a 36-month average of the Pool A Unit Market Value (UMV). Over the years, MIT has kept the “voted” distribution rate within the target range.

However, our “all-in” or effective distribution rate, which includes the additional endowment distribution as well as the voted endowment distribution, has been in the neighborhood of 5.5% since FY1999 (see Figure 5). The “Financial Foundation for the Future” strategy will drop the total, “all-in” distribution rate to 5.1% in FY2008, a rate that is consistent with the preservation of our assets for future generations (see Figure 5). It is important to emphasize that this does not reduce the funds that a DLC or faculty member will receive now or in the future.

Beyond FY08: Assessing the Future

The goal of this new financial strategy is to balance MIT’s operations and increase our financial flexibility for MIT’s future. Implementation of this strategy will require a great deal of commitment, collaboration, and hard work from faculty and administrative leaders across the academic units receiving GIB funds and holding endowed funds. By working together, we will lay a sound and sustainable financial foundation for MIT’s continued academic excellence.

| Back to top | |

| Send your comments |

| home this issue archives editorial board contact us faculty website |