Since we are all

sitting in front of computer screens, it is worth talking a bit about how

Brownian motion is studied in these machines!

Technically, one

can say that the numerical construction of a Brownian motion can be done in two

ways

·

As a

scaled random walk

·

In terms

of random Fourier series

WHAT???

OK, you are

right to be complaining, this sounds confusing!

Let’s just try

to understand the first of the two alternatives.

I’ll first give

you the definition and then the recipe and the results.

Definition:

Brownian motion

may be considered as a scaled version of the usual random walk on the lattice

with probability ½ to make aleft move and ½ to make a right move. In the limit where

the jumps take place every dt and the length of the jumps are dx, where dt goes

to 0, dx goes to 0 AND dx2/dt goes to 1, using (something called)

Central Limit Theorem, we may show that this random walk tends to the Brownian

motion.

OK, but how do

we actually do it?

The following

short algorithm solves this problem

for i=1:N

dW(i)=sqrt(dt)*rand

W(i+1)=W(i)+dW(i)

end

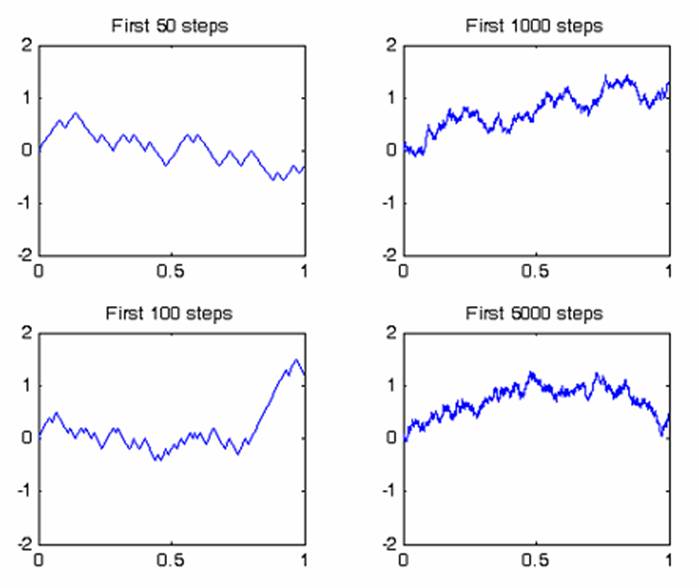

Let’s see what

the algorithm means: dW(i) contains the increments of the Brownian motion, rand

is a random number and W(i) contains the Brownian motion at time interval “i”.

Now let’s see

what we get!

Voila!