|

Airline Industry Overview

The international airline industry provides service to virtually every corner of the globe, and has been an integral part of the creation of a global economy. The airline industry itself is a major economic force, both in terms of its own operations and its impacts on related industries such as aircraft manufacturing and tourism, to name but two. Few other industries generate the amount and intensity of attention given to airlines, not only among its participants but from government policy makers, the media, and almost anyone who has an anecdote about a particular air travel experience.

During much of its development, the global airline industry dealt with major technological innovations such as the introduction of jet airplanes for commercial use in the 1950s, followed by the development of wide-body “jumbo jets” in the 1970s. At the same time, airlines were heavily regulated throughout the world, creating an environment in which technological advances and government policy took precedence over profitability and competition. It has only been in the period since the economic deregulation of airlines in the United States in 1978 that questions of cost efficiency, operating profitability and competitive behavior have become the dominant issues facing airline management. With the US leading the way, airline deregulation or at least “liberalization” has now spread to much of the industrialized world, affecting both domestic air travel within each country and, perhaps more importantly, the continuing evolution of a highly competitive international airline industry.

Today, the global airline industry consists of over 2000 airlines operating more than 23,000 aircraft, providing service to over 3700 airports. In 2006, the world’s airlines flew almost 28 million scheduled flight departures and carried over 2 billion passengers [1]. The growth of world air travel has averaged approximately 5% per year over the past 30 years, with substantial yearly variations due both to changing economic conditions and differences in economic growth in different regions of the world. Historically, the annual growth in air travel has been about twice the annual growth in GDP. Even with relatively conservative expectations of economic growth over the next 10-15 years, a continued 4-5% annual growth in global air travel will lead to a doubling of total air travel during this period.

In the US airline industry, approximately 100 certificated passenger airlines operate over 11 million flight departures per year, and carry over one-third of the world’s total air traffic – US airlines enplaned 745 million passengers in 2006. US airlines reported over $160 billion in total revenues, with approximately 545,000 employees and over 8,000 aircraft operating 31,000 flights per day [2]. The economic impacts of the airline industry range from its direct effects on airline employment, company profitability and net worth to the less direct but very important effects on the aircraft manufacturing industry, airports, and tourism industries, not to mention the economic impact on virtually every other industry that the ability to travel by air generates. Commercial aviation contributes 8 percent of the US Gross Domestic Product, according to recent estimates [3].

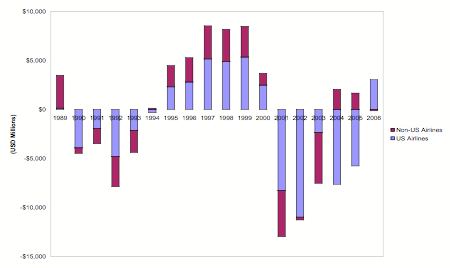

The economic importance of the airline industry and, in turn, its repercussions for aircraft manufacturers, makes the volatility of airline profits and their dependence on good economic conditions a serious concern for both industries. This concern has grown dramatically since airline deregulation, as stable profits and/or government assistance were the rule rather than the exception for most international airlines prior to the 1980s. As shown in Figure 1, the total net profits of world airlines have shown tremendous volatility over the past 15 years. After the world airline industry posted 4 consecutive years of losses totaling over $22 billion from 1990 to 1993, as a result of the Gulf War and subsequent economic recession, it returned to record profitability in the late 1990s, with total net profits in excess of $25 billion being reported by world airlines from 1995 to 1999. Even more dramatic was the industry’s plunge into record operating losses and a financial crisis between 2000 and 2005, with cumulative net losses of $40 billion.

FIGURE 1: WORLD AIRLINE NET PROFITS 1989-2006

Deregulation and Liberalization Worldwide

Since the deregulation of US airlines in 1978, the pressure on governments to reduce their involvement in the economics of airline competition has spread to most of the rest of the world. The US experience with airline deregulation is perceived to be a success by other countries, as the overall benefits to the vast majority of air travelers have been clearly demonstrated. While US domestic air travel grew at rates significantly greater than prior to deregulation, average real fares declined since deregulation and today remain at less than half of 1978 levels [2]. Several successful new entrant and low-fare airlines had a great impact both on airline pricing practices and on the public’s expectations of low-priced air travel. And, despite worries at the time of deregulation that competitive cost pressures might lead to reduced maintenance standards, there is no statistical evidence that airline safety deteriorated.

At the same time, the US deregulation experience had some potentially more negative impacts. The pressure to cut costs, combined with increased profit volatility, mergers and bankruptcies of several airlines led to periodic job losses, reduced wages and airline labor unions with less power than they previously enjoyed. Furthermore, the benefits of deregulation were not enjoyed equally by all travelers. Residents of small US cities saw changes in the pattern of air service to their communities, as smaller regional airlines replaced previously subsidized jet services. And, despite a substantial decrease in the average real fare paid for air travel in US domestic markets, the disparity between the lowest and highest fares offered by airlines increased, aggravating business travelers forced to pay the higher fares. The development of large connecting hubs by virtually all US major airlines also raised concerns about the pricing power of dominant airlines at their hub cities.

The management strategies and practices of airlines were fundamentally changed by deregulation, liberalization and, very simply, competition. Cost management and productivity improvement became a major focus of US airlines for much of the past twenty years, and non-US airlines have more recently been forced by competitive realities to face up to this challenge as well. A by-product of the quest for lower costs and increased productivity has been the pursuit of economies of scale by both US and non-US airlines. In the past, internal growth and/or mergers were the primary ways in which airlines hoped to take advantage of scale economies. With growing government concerns about industry consolidation, further mergers have become less likely. The response of airlines has been to expand their networks and to achieve at least some economies of scale through partnerships and “global alliances” designed to offer a standardized set of products and to project a unified marketing image to consumers.

Recent Industry Evolution 2000-2005

On a global scale and especially in the United States, the airline industry has been in a financial crisis for much of this new century. The problems that began with the economic downturn at the beginning of 2001 reached almost catastrophic proportions after the terror attacks of September 11, 2001. In the United States alone, the industry posted cumulative net losses of over $40 billion from 2001 to 2005, and only in 2006 was it able to return to the black with a total net profit of just over $3 billion [2].

The industry crisis was most certainly exacerbated by the events of 9/11, which resulted in immediate layoffs and cutbacks of almost 20% in total system capacity, in anticipation of the inevitable decline in passenger traffic due to concerns about the safety of air travel. However, the airlines were in serious trouble well before 9/11, as the start of an economic downturn already had negatively affected the volume of business travel and average fares. At the same time, airline labor costs and fuel prices were increasing yearly. To make matters worse, airlines were faced with deteriorating labor/management relations, aviation infrastructure constraints that led to increasing congestion and flight delays, and dissatisfied customers due to perceptions of poor service in general.

Thus, we cannot attribute the recent poor performance of the airline industry solely to the impacts of 9/11. In fact, the events of 9/11 actually provided a temporary reprieve from some of the industry's fundamental problems: Reductions in flight schedules alleviated some of the pressure on the aviation infrastructure, resulting in fewer flight delays; faced with massive layoffs and tremendous uncertainty about the financial futures of the airlines, labor unions moved towards a more conciliatory position, and passengers became more willing to lower their service expectations in exchange for improved security. In the period after 9/11, passenger traffic made a slow recovery, and returned to pre-9/11 levels by mid-2004. With total US domestic airline capacity substantially lower than before 9/11, average load factors soared to historical record levels. Yet, despite operating flights that were quite full, the large network airlines were still losing money.

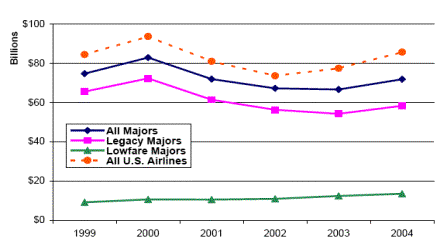

The ability of the network airlines to generate adequate revenues to cover their operating costs was severely impacted by major shifts in passenger choice behavior, particularly on the part of business travelers. The overall volume of business air travel demand decreased in early 2001 due to the overall economic downturn. Business air travel was further affected by the increased “hassle factor” and greater uncertainty in passenger processing times caused by increased security requirements. The combination of reduced business travel budgets and substantial cutbacks in airline passenger service quality led more business travelers to look for alternatives to paying premium air fares – teleconferencing and other travel substitutes, alternative travel modes, and especially, low-fare airlines for business travel. As a result, total US airline industry passenger revenues dropped by over 20% between 2000 and 2002, and were still 10% below 2000 levels in 2004, as shown in Figure 2.

FIGURE 2: US AIRLINE INDUSTRY PASSENGER REVENUES 1999-2004

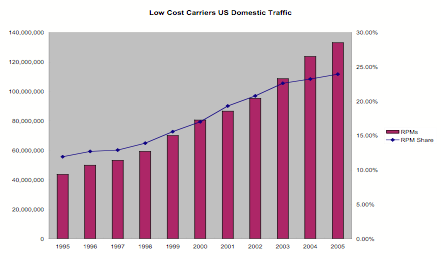

The recent growth of low-fare air travel options combined with a reduced willingness on the part of business travelers to pay the higher air fares charged by network carriers played a major role in contributing to the poor financial performance of traditional network airlines, both in the US and in many other countries. In the US, low-fare airlines (also known as Low Cost Carriers or “LCCs”) exhibited slow but steady growth since deregulation, but low-fare carriers accounted for less than 7% of US domestic air passengers in 1991. As shown in Figure 3, LCCs grew more rapidly in the US since the mid-1990s, to the point that they carried 25% of all US domestic traffic as a group in 2005 [4]. The largest low-fare airlines in the US industry include Southwest, JetBlue, AirTran, and Frontier.

While it is true that the network airlines encountered a serious “revenue problem” in the several years after 2001, it also became clear that they also had fundamental operating cost and productivity problems, when compared to their low-fare challengers. The differences in the cost structures between network airlines and low-fare carriers reflected substantial differences in the productivity of both aircraft and employees. Low-fare carriers typically operate “point-to-point” networks in which they can minimize aircraft ground times, in contrast to the hub-and-spoke networks of the largest legacy airlines. Shorter ground times translate directly into higher aircraft utilization rates. In 2004, JetBlue operated its Airbus 320 aircraft on average for 13.6 block hours per day, an aircraft utilization rate 46% higher than Northwest for the same aircraft type, and highest of all US Major airlines. At the same time, JetBlue's unit aircraft operating cost for this aircraft fleet was 3.2 cents per available seat mile (ASM), less than two-thirds of that reported by Northwest [4].

FIGURE 3: LOW COST CARRIERS US DOMESTIC TRAFFIC

Perhaps the most critical element of the successful low-fare airline business model is significantly higher labor productivity than traditional network carriers. The differences lie in labor productivity, not in unionization or even wage rates. Southwest is the most heavily unionized US airline and its salary rates are considered to be at or above average compared to the US airline industry. The low-fare carrier labor advantage is in much more flexible work rules that allow cross-utilization of virtually all employees (except where disallowed by licensing and safety standards). Such cross-utilization and a long-standing culture of cooperation among labor groups translate into lower unit labor costs. At Southwest in 2004, total labor expense per ASM was 25% below that of Delta [4].

Carriers like Southwest have a tremendous cost advantage over network airlines simply because their workforce generates more output per employee. In 2004, Southwest produced 3.2 million available seat-miles per employee, as compared to 2.2 million at American. By this measure, the productivity of Southwest employees was 45% higher than at American, despite the substantially longer flight lengths and larger average aircraft size of the network carrier.

Re-Structuring and a Return to Profitability in 2006

The challenges described above led four out of the six US Legacy carriers (US Airways, United, Delta and Northwest) into Chapter 11 bankruptcy between 2001 and 2005. Under bankruptcy protection, these carriers were able to focus on down-sizing, cutting operating costs and improving productivity as part of their re-structuring efforts. And, the other two Legacy carriers, American and Continental, used the threat of bankruptcy filing to do the same. Much of their cost-cutting strategy focused on labor: Legacy airline employment was reduced by 30% in just five years, representing over 100,000 jobs lost while average wage rates were also cut by 7% [4]. At the same time, the Legacy airlines sought productivity gains not only by reducing headcount, but also by introducing new technologies (e.g., internet ticket distribution, web check-in) and by moving capacity from domestic to international routes in an effort to improve aircraft utilization with increased stage lengths. Legacy carriers also attempted to mimic several strategies of the Low Cost Carriers (LCCs), for example, by eliminating meals and pillows to reduce costs and by reducing aircraft turn-around times to improve aircraft productivity.

LCCs in many respects took advantage of the weaknesses of the Legacy carriers during their financial crisis and re-structuring. Most LCCs were able to rapidly expand their networks and captured significant market share. They expanded into new markets with new aircraft, more flights and, of course, lower fares. However, during this same period the LCCs began to face increasing operating costs, driven by aging fleets and personnel with increasingly more seniority. And, the LCCs could not escape the impacts of more than a doubling in fuel costs between 2003 and 2005 – even the successful fuel hedging strategy of Southwest provided only a temporary reprieve from increasing fuel costs.

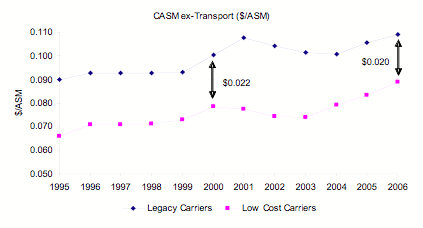

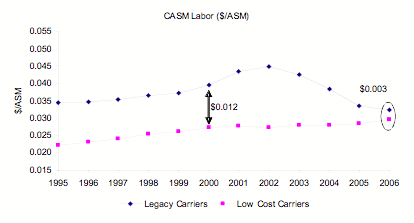

In fact, the concerted cost-cutting efforts of both Legacy and LCC airlines were not enough to offset the increased fuel prices, resulting in growing total unit costs for both airline groups (Figure 4) from 2001 to 2006. However, while total unit costs continued to increase due primarily to the impact of higher fuel prices, labor unit costs showed a very different trend – they have decreased dramatically for Legacy airlines, while they continue to increase among LCCs. As shown in Figure 5, there has been a clear labor cost convergence between both groups and the historical advantage that LCCs have had in this category was effectively eliminated by 2006. Indeed for the first time in 2006, LCC employees had on average a higher total compensation and benefits than their Legacy counterparts. Amazingly, the carrier with the highest labor expense per employee among Legacy and LCC airline in 2006 was Southwest [5].

FIGURE 4: UNIT COSTS (excluding Transport-related payments to regional carriers)

FIGURE 5: LABOR UNIT COSTS

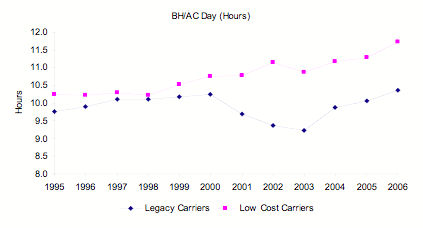

In terms of aircraft productivity, the Legacy carriers also made big gains, stemming in large part from the shift of larger and longer-range aircraft to international routes. Domestically, they tried to replicate the productivity strategies of LCCs, by eliminating fixed connecting banks at many hubs and moving to “continuous” or “rolling” banks that shortened aircraft ground times. Still, despite all of their efforts to improve aircraft productivity, the Legacy carriers have not been able to match the utilization rates (block hours per day of aircraft operation) that LCCs have been achieving (Figure 6). For example, Southwest and Jet Blue continue to hold a clear advantage in this measure of productivity [5]

FIGURE 6: AIRCRAFT UTILIZATION RATES (Block Hours per Aircraft per day)

In summary, the cost and productivity improvements by Legacy airlines have changed the competitive environment of the US airline industry yet again – there is much evidence of recent cost and productivity convergence between the Legacy and LCC airlines. Passenger traffic rebounded to exceed pre-9/11 levels by over 14% in 2006. The profitability results for 2006 were positive for most Legacy airlines, while several LCCs struggled financially. The US industry as a whole posted an aggregate net profit of $3 billion (excluding restructuring and bankruptcy costs). The painstaking restructuring efforts and cost-reductions of the Legacy airlines appear to be paying off, as the US industry is expected to post a $4 billion net profit in 2007 [6]. The industry has also benefited from an improving revenue environment and from little or no growth in available capacity (ASMs), particularly in US domestic markets.

Looking Ahead: Industry Challenges

The airline industry is in the midst of a dramatic restructuring that involves even more fundamental changes than those experienced following its deregulation in 1978. Yet, nearly three decades after deregulation – and after multiple cycles of financial successes and failures – the industry remains fragile. Competitive pressure from low-cost carriers, the loss of consumer confidence in the air transportation system’s reliability and operating performance, and the transparency of pricing facilitated by the internet and online travel distribution channels have all contributed to a precipitous decline in average fares and a significant impact on airline revenues.

And since 2006, fuel has emerged as the single largest industry expense, surpassing labor costs for the first time [4]. The industry still is recovering from its latest cycle of financial struggles, but faces substantial challenges. The belief that a few quarters of profits equate to full recovery is more wishful thinking than reality.

The next round of labor negotiations may be the most important milestone in the US airline industry since deregulation. The recent round of labor negotiations and restructurings – many under Chapter 11 – led to significant changes in labor costs and productivity. With those changes, airline employees helped contribute to the short-term recovery of the industry. Finding a new model for compensation that is durable and works to address the cyclicality of the industry will be critical. Just as important will be the efforts of management to identify non-labor cost savings that can be sustained as networks and operating models are reconfigured.

While there has been much progress on issues of aviation safety and security since 9/11, with the “federalization” of airport passenger screeners and movement towards explosives screening for all checked baggage, the questions “are we doing enough?” and “are we doing the right things?” remain unanswered. Demand for air travel, particularly in short-haul markets, has been suppressed by passenger perception of the “hassle factor” of increased security and the uncertainty of passenger processing times at the airport. For the airlines, the new security procedures have increased operating costs and induced more security-related flight disruptions and delays. The Director-General of IATA, the world-wide airline industry trade association, has said “our passengers have been hassled for 6 years…that’s far too much” [7]. Some experts, however, have expressed concern that cutbacks in existing security measures could increase the risk of future terrorist acts that could devastate the industry.

The temporary reprieve from congestion and flight delays experienced immediately after 9/11 has effectively ended at the nation's busiest airports. The number of delayed flights reached record levels in July 2007, and media reports of chronic and excessive airline passenger delays have again become commonplace. Several factors, including the lack of coordination of airline flight schedules at some of the most congested airports; an outdated air traffic control system; finely-tuned airline flight schedules with little slack to dampen delay propagation; and record-high load factors preventing timely re-accommodation of passengers who misconnect or whose flights are canceled, all combine to create passenger disruptions and lengthy passenger delays that exceed even the record-high levels of flight delays. Solutions to the problem will require a mix of improved management of airspace and airport demand, and an increase in airport capacity brought about primarily by improved management and utilization of existing capacity.

The lack of adequate infrastructure capacity – airports and airspace – and the rapidly growing costs of maintaining and expanding this infrastructure are two of the most critical problems for the future of air transportation, nationally and internationally. The prospects for substantial relief on the capacity front are not good – at least in the medium term (next 10 years). While the FAA and other air navigation service providers around the world have been working, with some success, toward increasing the capacity of the en route airspace, the real bottlenecks of the air transportation system are the runway systems of the major commercial airports in North America, Europe and Asia and the terminal airspace around them. The only clear way to increase the runway system capacity at these airports substantially, i.e., at rates similar to those at which demand is growing, is through the construction of new runways at existing airports or additional airports in the same metropolitan areas. But obtaining approval for and eventually opening additional runways and new airports is an extremely difficult and time-consuming proposition in most developed countries. Barring these, airports and national civil aviation authorities may have to resort to increasingly stringent “demand management” measures, such as slot restrictions, congestion pricing, and even the auctioning of access to major airports.

On the cost side, the enormous investments required in order to expand and maintain the capacity of existing airports or to build new ones has been one of the main reasons for the airport privatization trend that has been in evidence in much of the world (but, for statutory reasons, not in the United States) since the late 1980s. A growing tendency to tax directly airline passengers and cargo is another consequence of the rapidly increasing costs of aviation infrastructure (airports and air traffic control). Various taxes and fees for infrastructure support and security currently increase the cost of the average domestic airline ticket in the United States by about 16%. The situation in the European Union is roughly the same.

These important challenges – sustaining airline profitability, ensuring safety and security, and developing adequate air transportation infrastructure – are not limited to the United States or to US airlines. Airlines around the world are encountering a growing wave of liberalization if not outright deregulation, and as a result are facing competitive pressures, both from new entrant low-cost airlines and re-structured legacy carriers. The rapid growth of the global airline industry and the continued threat of terrorist attacks make safety and security issues critical to every airline, and every airline passenger. And, the need for expanded aviation infrastructure, both airports and air traffic control, is of particular importance to emerging economies of the world such as India, China, Africa and the Middle East, where much greater rates of demand growth are forecast for both passenger and cargo air transportation.

REFERENCES

[1] International Air Transport Association (IATA), Fact Sheet: World Industry Statistics, www.iata.org.

[2] Air Transport Association of America (ATA), 2007 Economic Report, www.airlines.org.

[3] Air Transport Association of America (ATA), Statement on the State of the Airline Industry, Statement for the Record of the Sub-committee on Aviation, Transportation and Infrastructure Committee, US House of Representatives, June 2004.

[4] US Department of Transportation Bureau of Transportation Statistics, Form 41 Airline Traffic and Financial Reports.

[5] G. Tsoukalas, “Convergence in the US Airline Industry: A Unit Cost and Productivity Analysis”, MIT Master’s Thesis, Department of Aeronautics and Astronautics, August 2007.

[6] J. Heimlich, “Outlook: Reaching for the Skies?”, Air Transport Association of America, www.airlines.org. January 2007

[7] G. Bisignani, “State of the Air Transport Industry”, Address to the Annual General Meeting, International Air Transport Association, Vancouver, June 2006, www.iata.org.