Overview

Fissile elements are mainly used in the generation of clean energy; however, their unifying ability is to break apart during fission. In a nuclear reaction, fission releases neutrons that split neighboring nuclei, inducing a sustained, energetic chain reaction; 1 kg of enriched uranium can create approximately 50,000kWh (kilowatt hours) of energy, over 16,000 times the amount produced by a comparable quantity of coal ("Uranium"). However, this highly efficient energy production does not come without costs. After a nuclear reaction dies down, what is left of the original fuel is highly radioactive. The spent fuel needs to be securely stored for a long amount of time (on the order of centuries), lest it has harmful effects on living organisms. Despite the issue of spent fuel, fission is by far the greenest method of energy production; it does not produce any greenhouse gases ("Uranium").

There are three radioactive isotopes that are fissile (able to undergo fission): plutonium-239, uranium-233, and uranium-235 (Stwertka, 1998). Plutonium is only produced as a by-product of fission of uranium; it shall not be discussed in depth, as it does not see wide use, except in nuclear weapons. Uranium and Thorium are the two most common radioactive elements. Thorium is much more common than Uranium; however, even with a plutonium core, technology has not reached the point where thorium fission reactions are self-sustaining (Dean, 2006). Thus, Uranium will be the main fission element under discussion because it is currently used in energy production and is produced through mining of parent oxides.

Although demand for fission elements has increased over the years, future demand growth is expected to be modest. Current mineable world reserves are expected to last for at least 70 years, if not 100 ("Global Uranium Supply", 2012). Thus, as will be explained in detail below, supply of fission elements is expected to be able to meet demand for most of the next century.

Current and Predicted Fission Element Demand

Current global uranium demand is estimated at 64,000 tonnes per annum ("Global uranium supply," 2012). Global thorium demand is close to zero. Numbers for plutonium demand are hard to find, as most plutonium is used in mixed oxide ("MOX") fuels for reactors, or in weapons. However, total demand is quite small, as military demand for nuclear weapons has practically halted (International Panel for Fissile Materials, 2012).

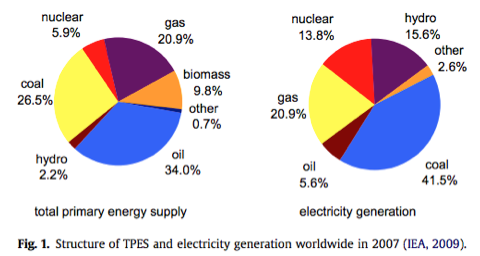

As fission elements are mainly used in energy production, it is important to look at predictions for future energy production when attempting to predict future fission element demand. The following chart (Yan, 2011) shows from which sources the world generates its electricity and energy; we can see that oil and coal are the biggest energy providers, and coal and gas are the largest electricity generators. Nuclear energy hovers at 6% for energy production and 14% for electricity generation.

However, both oil and coal are major producers of greenhouse gases. Recently, numerous studies and public awareness campaigns inspired a "green" movement away from these energy sources. As the coal and oil slices of the pie shrink, and technology and safety features of nuclear power improve, the nuclear slice will only grow larger ("Global uranium supply," 2012).

According to a joint Nuclear Energy Agency and International Atomic Energy Agency (NEA-IAEA) Secretariat study, nuclear energy production is projected to grow between 44% and 99% from 2010 to 2035 (from 375 to 540-746 GWe). Uranium demand is therefore predicted to rise from 64,000 tonnes to 98,000-136,000 tonnes ("Global uranium supply," 2012). However, these predictions for uranium demand do not take thorium fission into consideration. Once thorium fission becomes technologically feasible, demand for uranium will greatly decrease. Thorium nuclear plants should produce radioactive waste with a shorter half-life than uranium nuclear plants, and would offer less possibility of a meltdown while keeping costs relatively low. India, which contains 25% of the world's thorium reserves, aims to meet 30% of its electricity demand through thorium-based reactors by 2050 (Bhattacharyya, 2011). If thorium energy production becomes feasible, then it is likely that it will reduce global demand for uranium, as thorium is more abundant, and produces less radioactive waste.

If thorium fission comes online, then demand for thorium will greatly increase; however, for the moment, the increase in demand cannot be predicted accurately because the technology does not exist (Dean, 2006). Thorium certainly has increased future use; the benefits of thorium energy production are simply too great for the technology not to be developed.

Current and Predicted Fission Element Supply

Currently, fission element supply either meets or is in excess of demand ("Global uranium supply," 2012). For thorium, there are large global reserves, but thorium currently isn't being produced except as a by-product of the mining of rare earth oxides and other ores. As thorium is already produced as a by-product of rare earth mining, there is high ability to readily expand supply (Bhattacharyya, 2011).

Plutonium does not exist in nature, but it is currently produced as a by-product of uranium fission. Global reserves for plutonium are around 500 tons, half of which are military reserves for weapons and nautical power (International Panel for Fissile Materials, 2012). Plutonium continues to be produced, recently Great Britain As of January 2011, uranium supply should be sufficient for over one hundred years, and current yearly supply is at consistent levels with demand ("Global Uranium Supply", 2012).

Equality Between Future Supply and Demand

As explained above, supply and demand for fission group elements are both increasing. Multiple studies have shown that future fission element supply will be more than enough to meet future demand. Projected growth in uranium supply is sufficient to meet even a 99% increased demand (the upper bound found by the NEA-IAEA). The NEA-IAEA study predicted that current uranium resources base "is more than adequate to meet high-case requirements through 2035 and well into the foreseeable future" ("Global uranium supply," 2012).

Current demand and the NEA-IAEA predictions paint a promising future for the matching of supply and demand, especially since they do not take into account possible thorium technology. Thus the supply and demand projections for fission elements do not require immediate intervention in fission element supply.

A different prediction by the Economics Department at Nantes University projects similar results. They used the NEA-IAEA study and their own projection models.

Their model "is estimated for three different time periods which take into account the major events that have influenced the nuclear-uranium development, that is, that have constrained the growth rate or nuclear generating capacity…" (Kahouli, 2011). It reaches the same conclusion: demand will not outstrip supply.

Thus, this project will not consider specific measures to moderate uranium supply or demand, because studies have spoken to their sustainability. Businesses and governments are already well-incentivized to continue research and development on their own, given the profitability of uranium. As for other fission elements, plutonium reserves are quite large. As plutonium is not widely used, and plutonium supply continues to increase as a result of uranium fission, it is unlikely that supply will fall behind future demand. For thorium, demand is expected to increase, however, supply has great ability to increase as well. Thus, it is unlikely that thorium demand will outstrip supply in the future (Bhattacharyya, 2011).

In conclusion, while demands for fission elements are expected to increase significantly over the next 100 years, global supply should easily meet such increases in demand.

Case Study: Changes in Supply and Demand Due to Nuclear Disaster

Reaction to the Fukushima disaster created an interesting case study for fission-element demand after a nuclear disaster. A disaster such as this is liable to happen with such unstable elements; Chernobyl and Three Mile Island were of even larger scale.

Fukushima led to a decrease in demand: 54 of Japan's 56 reactors closed, removing about 18 million pounds of demand per year. Germany, reacting to public outcry about safety, cut 17 reactors, removing an additional 3 million pounds of demand ("Uranium one sees," 2012).

However, this decrease in demand was matched by a decrease in supply. "Industry participants have already factored the Fukushima effect into market prices," and the effect ended up being small over time. Although the aftermath of Fukushima witnessed a dampening in prices, uranium prices were 10 USD/pound higher than they had been one year before one year following the Japanese tsunami ("Uranium One Sees," 2012).

It can be concluded from this example that disasters will not significantly affect either supply or demand.

Bhattacharyya, K. (2011, March 24). Indian thorium breeding technology. Retrieved from

http://large.stanford.edu/courses/2011/ph241/bhattacharyya1/

Dean, T. (2006, April). New age nuclear. Retrieved from

http://www.cosmosmagazine.com/features/print/348/new-age-nuclear?page=0,2

Global uranium supply ensured for long term, new report shows. (2012, July 26). Retrieved from

http://www.iaea.org/newscenter/pressreleases/2012/prn201219.html

Kahouli, S. (2011, January). Re-examining uranium supply and demand: New insights. Retrieved

from http://www.sciencedirect.com/science/article/pii/S0301421510007573

Stwertka, A. (1998). A guide to the elements. (Revised ed.). New York: Oxford University Press,

Inc.

Uranium. (n.d.). Retrieved from http://www.ggg.gl/uranium/

Uranium one sees continued demand growth; uranium price recovering after fukushima. (2012,

March 6). Retrieved from http://www.i-nuclear.com/2012/03/06/uranium-one-sees-continued-demand-growth-uranium-price-recovering-after-fukushima/

Yan et al. (2011, August). Nuclear power development in china and uranium demand forecast:

Based on analysis of global current situation. Retrieved from http://www.sciencedirect.com/science/article/pii/S0149197010001411